Chapter 14: Commodity taxation

Chapter summary

Commodity taxes are imposed upon purchases of goods. Such transactions are generally public information so making them a good target for taxation. The drawback is that the taxes drive a wedge between the price producers receive and the price consumers pay. This leads to inefficiency and reduces the attainable level of welfare compared to what could be achieved using lump-sum taxes. This is the price that has to be paid for incentive-compatible taxation. The imposition of a tax raises the price of a good. On the consumer side of the market, the analysis of income and substitution effects predicts what will happen to demand. For producers, the tax is a cost increase and they respond accordingly. What is more interesting is the choice of the best set of taxes for the government. Such optimal taxes raise a given level of government revenue while minimising the efficiency costs. This is the Ramsey problem of efficient taxation, first addressed in the 1920s. More general problems introduce equity considerations in addition to those of efficiency. The chapter begins by presenting a diagrammatic analysis of optimal commodity taxation. This is then used to demonstrate the Diamond-Mirrlees Production efficiency lemma. Following this, the Ramsey rule is derived and an interpretation of this is provided. The extension to many consumers is then made and the resolution of the equity/efficiency trade-off is emphasised. This is followed by a review of some numerical calculations of optimal taxes based on empirical data.

14.1 Optimal commodity taxation

Optimal commodity taxes attain the highest level of welfare possible whilst raising the revenue required by the government. In setting the taxes, consumers must be left free to choose their most preferred consumption plans at the resulting prices and firms to continue to maximise profits. The

taxes must also lead to prices which equate supply to demand.

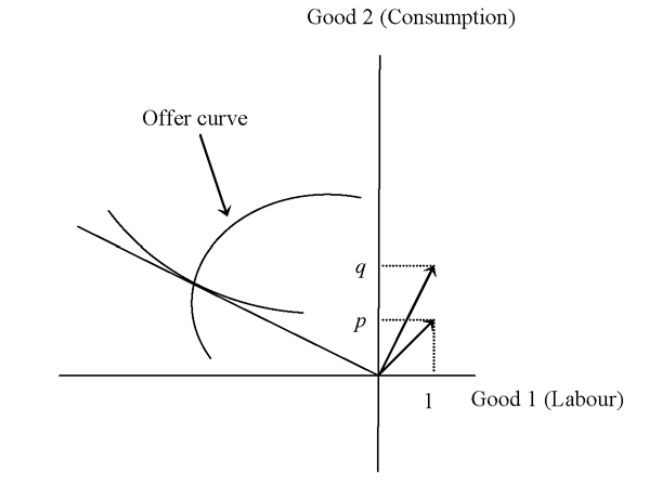

The budget constraint for the consumer is constructed by setting the consumer’s price for the output to q. The difference between q and p is the tax upon the consumption good. It should be noticed that labour is not taxed but this is not a restriction on the set of possible taxes. With these prices, the consumer’s budget constraint can be written qx = gamma where x denotes units of the output and gamma units of labour.

Varying the price q gives a series of budget constraints whose slopes increase as q falls. Forming the locus of optimal choices for each budget constraint traces out the consumer’s offer curve. The interpretation given to the offer curve is that the points on the curve are the only ones

consistent with utility maximisation by the consumer in the absence of lump-sum taxation. It should also be noted that the consumer’s utility rises as a move is made up the offer curve.

This discussion has shown how the optimal commodity tax is determined at the highest point of the offer curve in the production set. This is the solution to the problem of finding the optimal commodity tax for this economy. The diagram also shows why labour can remained untaxed without affecting the outcome. The choices of the consumer and the firm are determined by the ratio of prices they face or the direction of the price vector. Changing the length (but not direction) of either p or q introduces a tax on labour but this does not alter the fact that e is the optimum. This reasoning can be expressed by saying that the zero tax on labour is a normalisation, not a real restriction on the system.

The highest attainable indifference curve for the consumer given the production set is I 1 and utility is maximised at e * . This point would be chosen by the consumer if they faced a budget constraint which was coincident with the production frontier. A budget constraint of this form would cross the horizontal axis to the left of the origin and would have the form qx = gamma-R where R represents a lump-sum tax equal to the revenue requirement. This lump-sum tax would decentralise the first-best outcome at e*. Commodity taxation can only achieve the second-best at e.

• Use of normalisation rule

• Optimum where offer curve crosses production frontier

• Commodity taxation is second best.

14.2 Production efficiency

The analysis of optimal taxation in the one-consumer economy also provides another important result. This result, known as the Diamond-Mirrlees Production efficiency lemma, states the production

must be efficient when the optimal taxes are employed. In other words, the optimum with commodity taxation must be on the boundary of the production set.

Production efficiency occurs when an economy is maximising the output attainable from its given set of resources. This can only happen when the economy is on the boundary of its production possibility set. In the special case in which each firm employs some of all of the available inputs, a necessary condition for production efficiency is that the marginal rate of substitution (MRS) between any two inputs is the same for all firms. Such a position of equality is attained, in the absence of taxation, by the profit maximisation of firms in competitive markets.

The Diamond-Mirrlees lemma provides a persuasive argument for the non-taxation of intermediate goods and the non-differentiation of input taxes between firms. These are results of immediate practical importance since they provide a basic property that an optimal tax system must possess. As will become clear, it is rather hard to make precise statements about the optimal levels of tax but what the efficiency lemma provides is a clear and simple statement about the structure of taxation.

• Definition of production efficiency

• Optimum with commodity tax is production efficient

• Non-taxation of intermediate goods.

14.3 The inverse elasticity rule

When there is more than one commodity the question arises of how the tax burden should be distributed across commodities. An argument occasionally met is that the best policy is to tax all commodities at the same rate since this leads to the least distortion in prices. However, what this argument misses is that it is the level of consumption that matters for welfare. Once this is taken into account, a very different conclusion emerges.

The inverse elasticity rule is derived by assuming that there is a single consumer and that the demand for each good is dependent only upon its own price and the wage rate. Consequently, there are no cross-price effects between the taxed goods. This independence of demands is a strong assumption so that it is not surprising that a clear result can be derived. Since there is a single consumer the tax system derived is an efficient one, not necessarily an equitable one.

To interpret the rule, it must be noted that alpha is the marginal utility of another unit of income for the consumer and gamma is the utility cost of another unit of government revenue. Since taxes are distortionary, gamma > alpha. The rule therefore states that the proportional rate of tax on good k should be inversely related to its price elasticity of demand.

Furthermore, the constant of proportionality is the same for all goods. These observations imply that necessities, which by definition have low elasticities of demand, should be highly taxed. The importance of this observation is reinforced when it is set against the alternative, but incorrect, argument that the optimal tax system should raise the prices of all goods by the same proportion in order to minimise the distortion caused by the tax system. This is shown by the inverse elasticity rule to be false.

• Efficient tax system

• No cross-price effects

• Tax inversely related to elasticity.

14.4 The Ramsey rule

The inverse elasticity rule assumes that the demand for each good is dependent only upon the price of that good. Relaxing this assumption makes it necessary to account for the cross-price effects in demand. The result of conducting the optimisation of welfare in this more general setting is called the Ramsey rule and is one of the oldest results in the theory of optimal taxation. It provides a description of the optimal taxes for an economy with a single consumer in which there are no equity

considerations.

What the Ramsey rule states is that (to a first approximation) the optimal tax system should be such that the compensated demand for each good is reduced in the same proportion relative to the pre-tax position. This result emphasises that it is the distortion caused by the tax system in terms of quantities, rather than prices, that should be minimised. Since it is the level of consumption that determines utility, it is not surprising that what happens to prices is secondary relative to what happens to quantities. Prices only matter in so far as they determine demands.

Returning to the general case, goods that are unresponsive to price changes are typically necessities such as food and housing. Consequently, the implementation of a tax system based on the Ramsey rule would lead to a tax system that would bear most heavily on these necessities. In contrast, the lowest tax rates would fall on luxuries. If put into practice, such a tax structure would involve low income consumers paying disproportionately larger fractions of their incomes in taxes relative to rich consumers.

The single-consumer framework is not accurate as a description of reality and leads to an outcome that is unacceptable on equity grounds. It shows how taxes are determined by efficiency considerations and hence gives a baseline from which to judge the effects of introducing equity.

• Ramsey rule generalises the inverse elasticity rule

• Optimality implies proportional reduction in compensated demand

• Necessities taxed more heavily.

14.5 Applications and equity

The first step to practical application is to introduce equity considerations into the setting of taxes. This is undertaken by assigning consumers different relative importance in the social welfare function.

The second step to practical policy is to develop a method for numerically implementing the rules for optimal taxation. Two basic pieces of information are needed in order to calculate the tax rates. The first is knowledge of the demand functions of the consumers. The second piece of information is the social valuations of each consumer. Ideally, these valuations should be calculated from a specified social welfare function and individual utility functions for the consumers.

In practice, the difficulties are circumvented rather than solved. The approach that has been adopted is to first ignore the link between demand and utility and then impose a procedure to obtain the social welfare weights.

• Equity moderates the Ramsey rule

• Optimal commodity taxes can include subsidisation

• Redistribution can be significant.

READING: Hindriks and Myles, Intermediate Public Economics, MIT, 2004

Chapter 14: Inequality and Poverty

Commodity taxes are levied on transactions involving the purchase of goods. The necessity for keeping accounts ensures that such transactions are generally public information. This makes them a good target for taxation. The drawback, however, is that their use introduces distortions into the economy. The taxes drive a wedge between the price producers receive and the price consumers pay. This leads to inefficiency and reduces the attainable level of welfare compared to what could be achieved using lump-sum taxes. p351

Lump-sum taxation was described as the perfect tax instrument becuase it does not cause any distortions. The absence of disortions is due to the fact that a lump-sum tax is defined by the condition that no change in behaviour can affect the level of the tax. Commodity taxation does not satisfy this definition. It is always possible to change a consumption plan if commodity taxation is introduced. Demand can shift from goods subject to high taxes to goods with low taxes and total consumption reduced by earning less or saving more. It is these changes at the margin, which we call substitution effects, that are the tax-induced distortions.

The introduction of a commodity tax causes raises tax revenue but causes consumer welfare to be reduced. The deadweight loss of the tax is the extent

to which the reduction in welfare exceeds the revenue raised. p352

The purpose of the analysis is to find the set of taxes which give the highest level of welfare whilst raising the revenue required by the government. The set of taxes that do this are termed optimal. In determining these taxes, consumers must be left free to choose their most preferred consumption plans at the re-sulting prices and firms to continue to maximize profits. The taxes must also lead to prices which equate supply to demand. This section will consider this problem for the case of a single consumer. This restriction ensures that only efficiency considerations arise.

p354

.. the Diamond-Mirrlees production efficiency lemma, states the production must be efficient when the optimal taxes are employed. In other words, the optimum with commodity taxation must be on the boundary of the production set. p359

Production efficiency occurs when an economy is maximizing the output attainable from its given set of resources. This can only happen when the economy is on the boundary of its production possibility set. Starting at a boundary point, no reallocation of inputs amongst firms can increase the output of one good without reducing that of another (compare this with the Pareto efficiency criteria of Chapter 7). In the special case in which each firm employs some of all of the available inputs, a necessary condition for production efficiency is that the marginal rate of substitution (M RS) between any two inputs is the same for all firms. Such a position of equality is attained, in the absence of taxation, by the profit maximization of firms in competitive markets. Each firm sets the marginal rate of substitution equal to the ratio of factor prices and, since factor prices are the same for all firms, this induces the necessary equality in the M RSs. The same is true when there is taxation provided all firms face

the same post-tax prices for inputs, that is, inputs taxes are not differentiated between firms. p359

... should all goods have the same rate of tax or should taxes be related to the characteristics of the goods? This section will provide a derivation of a formula that goes a long way to answering this question. This formula is called Ramsey rule and is one of the oldest results in the theory of optimal taxation. It provides a description of the optimal taxes for an economy with a single consumer in which there are no equity considerations.

p363-364

the Ramsey rule can be interpreted as saying that the optimal tax system should be such that the compensated demand for each good is reduced in the same proportion relative to the pre-tax position. This is the standard interpretation of the Ramsey rule. p366

The importance of this observation is reinforced when it is set against the alternative, but incorrect, argument that the optimal tax system should raise the prices of all goods by the same proportion in order to minimize the distortion caused by the tax system. This is shown be the Ramsey rule to be false. What the Ramsey rule says is that it is the distortion in terms of quantities, rather than prices, that should be minimized. Since it is the level of consumption that actually determines utility, it is not surprising that what happens to prices is secondary to what happens to quantities. Prices only matter so far as they determine demands. p366