Chapter 2: The IS–LM model

Aims of the chapter

The focus of the chapter is on the IS–LM model ["investment-savings" (IS) and "liquidity preference-money supply" (LM)], set out by Hicks (1937) in response to Keynes’ The general theory of employment, interest and money (1936) for analysing the aggregate demand and macroeconomic stabilisation policy in a closed economy and with fixed prices. The IS–LM model integrates the goods and the money markets and considers under what conditions output and the interest rate are simultaneously in equilibrium; what factors may determine short-run fluctuations; and how macroeconomic policy can be employed to stabilise the economy in the short run.

• list and discuss the key equations of the IS–LM model

• describe the determinants of the intercept and the slope of both the IS and the LM curves

• calculate the equilibrium level of output and the interest rate in a closed economy with fixed wages and prices

• evaluate how any change in the variables and the parameters of the IS–LM model alters the equilibrium levels of output and the interest rate

• show how fiscal and monetary policies contribute to the determination of output and the interest rate in the short run, and their use as tools for macroeconomic stabilisation

• illustrate and exlain the Keynesian view of short-run fluctuations in economic activity.

Introduction

The IS–LM model combines the goods market, which determines the equilibrium level of output, with the money market, which determines the equilibrium level of real money, in order to determine under what conditions they are simultaneously in equilibrium, and to assess the role that fiscal and monetary policies may have in explaining real output fluctuations.

The model focuses on the assessment of aggregate demand in the short run, and in a closed economy. The short run is defined as the period of time during which the price level is fixed (there is no inflation), in the sense that it does not change in response to variations in other macroeconomic variables. Recall that the price level can be thought of as sluggish or sticky variable, since it does not respond immediately to a macroeconomic disturbance. Instead the adjustment builds up gradually, and it is fully completed after several years. In this respect, the long run is a period of time long enough for prices to be considered fully flexible, whereas the medium run is the period of time over which the price level completes its adjustment to macroeconomic disturbances. The closed

economy assumption means that the model is studied without taking into account the effect of foreign trade on domestic aggregate demand.

Therefore, the IS–LM model is useful in analysing the effects of stabilisation policy on real output and the real interest rate, but it cannot be employed to assess issues related to inflation, long-run unemployment, and the exchange rate. Because great attention is given to fiscal policy, it is important that you have a clear understanding of some basic assumptions about the role of the government in the economy, the links existing among different fiscal variables, and the standard fiscal policy jargon. Here is a quick summary. The government provides public goods and services (e.g. health, education, roads, defence) that the private sector would either under-produce or not produce at all. The government also redistributes resources among households and firms. These activities can be financed either by levying taxes on households and firms, or by issuing debt, or by issuing money. The relationship between public spending, taxes, debt and money is summarised by the government budget constraint (GBC), an accounting identity that for every generic period t can be written as:

G_t + i_t B_t–1 – T_t = ∆B_t + ∆M_t

where G_t is government spending in goods and services during year t; B_t–1 is government debt at the end of year t–1 or, equivalently, at the beginning of year t; i_t B_t–1 measures the interest payments on government debt made by the end of period t at the interest rate i_t ; 1 T_t computes tax revenue net of transfers to households and firms during year t; the term ∆B t = B_t – B_t–1 is the change in debt during year t; and the term ∆M_t = M_t – M_t–1 is the change in money supply during year t. In the rest of this chapter we will assume that the government cannot create money to finance

public spending, hence we will set ∆M_t = 0.

The difference between government spending and tax revenue, G_t – T_t , is referred to as the primary budget deficit. The term G_t + i_t B_t–1 – T_t is instead called the total budget deficit, as it includes interest spending. The standard interpretation of the GBC is that any difference between total spending and tax revenue must be balanced with a corresponding change in the stock of debt. The government runs a balanced primary budget when public spending is entirely financed through taxes, that is G_t = T_t .

We say that a balanced budget expansion or contraction of the fiscal sector occurs when taxes and government spending either increase or decrease by the same amount.

The IS–LM model: key assumptions

The IS–LM model determines under what conditions output and the interest rate are simultaneously in equilibrium in the short run.

Output is determined in the goods market, which refers to the trade market of all goods and services produced in an economy. The goods market equilibrium is described under the following assumptions:

• All firms produce the same goods, which are then used by consumers for consumption and residential investment, by firms for fixed assets investment, or by the government.

• Firms are willing to supply any amount of goods at the existing price level.

• The economy is closed.

The second assumption is important because it implies that in the IS–LM model aggregate supply has no effect on the equilibrium level of income, which is determined by aggregate demand.

The interest rate is determined in the money market. The Keynesian Liquidity Preference theory, which you have already encountered in describes money market equilibrium under the following assumptions:

• The financial market includes only two assets: money and bonds.

• Money is a liquid asset, in the sense that it can be used to purchase goods and services, and pays no interest.

• Bonds are issued by the government, cannot be used for transactions, but pay a positive nominal interest rate i.

• Real wealth is fixed in the short run.

Bonds are defined as assets that pay a fixed amount of money (face value) at a specific period of time (maturity). Individuals buy bonds at a price lower than the face value. The difference between the price and the face value of a bond is the gain for the bond holder. Since the face value is fixed, the lower the price of a bond the higher is the gain for the holder. The rate of return from investment in bonds, the nominal interest rate, is calculated by dividing the gain from bonds by the current price. Analytically, the relationship between the interest rate and the price of a

bond is written as:

i = FP_B − P_B/P_B = (FP_B/P_B) -1

where FP_B indicates the face value of the bond and P B is the current price of bonds. Thus, the interest rate and the price of bonds are, by construction, inversely related: an increase in the price of bond, P_B , is equivalent to a reduction in the interest rate.

It is important that you clearly understand the difference between income and wealth. Individuals earn income essentially from three sources: labour, in the form of wages, real assets, in the form of rent, and financial assets, in the form of interest and dividends. Income can either be spent to purchase goods and services or saved to buy new assets. Wealth is defined as the net value of all assets held by an individual, including their human capital. If the level of consumption of an individual exceeds their income, then this individual is defined as a net borrower.

Finally, it is important that you note the equilibrium conditions in the financial market. These state that the demand for money, M^d , must be equal to the supply of money, M^s :

M^d = M^s

and that the demand for bonds, B^d, must be equal to the supply of bonds, B^s:

B^d = B^s

In general, we know from Walras’ law that if there are n markets and the first n–1 of these are in equilibrium, then the nth market must be in equilibrium too. This means that we can choose to ignore one market in the model, knowing that equilibrium there will be assured whenever it holds generally elsewhere. For this reason, we ignore the bond market in what follows, and make use only of the money market equilibrium condition.

The IS–LM model: behavioural equations and identities

The IS–LM model is based upon six behavioural equations, each describing the determinants of one of the macroeconomic variables considered by the model: consumption, investment, tax revenue, government spending, money demand and money supply.

Consumption, C, is defined as the value of goods and services purchased by households. The linear consumption function, which depends positively on income, Y, and negatively on taxes, T, can be written as:

C = c0 + c1(Y–T) c0 ≥ 0, 0 < than c1 < 1

where the term Y–T indicates disposable income. The parameter c0 measures the level of consumption affected by factors other than disposable income, such as borrowing, sale of real and financial assets, etc. The value of c0 depends also upon consumers’ spending habits and consumer confidence about current and future spending opportunities.

The parameter c 1 is the marginal propensity to consume. In turn, the value 1– c 1 measures the marginal propensity to save. Since 0 < c1 < 1, an increase in disposable income cannot be either entirely saved, c1 = 0, or entirely consumed, c1 = 1

Investment spending includes three broad categories: fixed business investment carried out by firms, residential investment carried out by households, and inventory investment (i.e. unsold goods and services and/or unused materials).

Demand for investment depends positively on income (sales) and negatively on the real interest rate, r, and it can be written as:

I = I+b1Y – b2r, b1 ≥ 0, b2 ≥ 0

Where Ī is a constant that computes the effect on investment of any variable other than income and the interest rate, whereas b1 and b2 measure the sensitivity of investment to income and the interest rate, respectively.

[Note that in economics, the symbol i normally indicates the nominal interest rate, whereas the symbol r is used to indicate the real interest rate.]

Nominal and real interest rates are linked by the Fisher equation: i = r + p which shows that the nominal interest rate is equal to the sum of the real interest rate and the rate of inflation, p.

Since the Keynesian theory assumes prices to be constant in the short run, the rate of inflation is equal to zero, which implies that the real and the nominal interest rates are equal in the short run, i = r. For this reason we can replace r with i in the demand for investment equation when solving the model.

Tax revenue depends upon the structure of the tax system (lum sum, Tfix, proportional income, proportional consumption) . The linear tax function can be written as:

T = Tfix + τ1Y + τ2C, τ1 ≥ 0, τ2 ≥ 0

This is an approximate version of the equation only.

Government spending refers to the demand for goods and services of the public sector and it can be generally described by the equation:

G = Gfix + g1Y + g2C ,

where Gfix represents the fixed component of government spending, while g1 and g2 measure changes in public spending proportional to variations in income and consumption, respectively.

The demand for money, Md , is positively related to income and negatively related to the nominal interest rate. The higher the level of transactions, the more money is demanded for consumption and investment by individuals, firms and the government. The interest rate can be regarded as the opportunity cost of holding money. The higher the interest rate, the higher is the cost of holding money rather than bonds, and thus the lower is money demand. Analytically, real money demand is described as:

M^d/Pfix = = h0 + h1Y − h2i, h1 ≥ 0, h2 ≥ 0

where P indicates the price level, which is constant in the IS–LM model, h0 measures the level of demand for money independent of income and the interest rate, and the parameters h1 and h2 measure the sensitivity of money demand to income and the interest rate respectively.

Note that equation shows that demand for money is ultimately a demand for real balances, M^d/Pfix , rather than nominal balances, M^d . The underlying assumption behind this specification is that individuals are free from money illusion, namely the tendency of individuals to think of currency in nominal terms rather than taking into account its purchasing power (**COMMENT** c.f., above on factors of production **COMMENT**).

The supply of money, Ms , is assumed to be independent from the interest rate and directly controlled by the central bank. The central bank can change money supply through open market operations. An expansionary open market operation occurs when the central bank buys bonds to increase the money supply. When the central bank buys bonds from the private sector, the excess demand for bonds raises the price of bonds, in turn reducing the interest rate. This reduction in the opportunity cost of holding money simutaneously increases money demand. In contrast, a contractionary open market operation occurs when the central bank sells bonds. As a result of excess supply the bond price falls, the interest rate increases, and money demand decreases.

Analytically, real money supply, MsSqrtP is written as:

Ms/P = M/P'

Where M is the level of nominal money supply chosen by the central bank.

Income accounting in a closed economy

The equilibrium output in the goods market can be alternatively retrieved from the equality between saving and investment in the loanable funds market. Consider again the income identity in equation (2.9):

Y = C + I + G.

Next, move C and G to the left-hand side of the equation and add and

subtract T to obtain:

(Y – T – C) + (T – G) = I.

The term on the left hand side is the total saving of the economy. In particular, S = Y – T – C indicates private saving, measured by the excess of income over taxes and consumption, whereas T – G is public saving, measured by the primary budget surplus. 8

Therefore, the equilibrium output in the goods market can be alternatively determined by the condition ‘saving equals investment’: (2.10)

S + T – G = I

At this stage, make sure you are familiar with the concept, already encountered in EC1002 Introduction to economics, of the ‘paradox of thrift’ (or ‘paradox of saving’) which states that an exogenous increase in saving, equivalent to lower consumption at any given income level, leads to a lower equilibrium level of output and unchanged aggregate saving so long as the interest rate stays constant.

Equation (2.10) gives an alternative way of writing the income identity in a closed economy, by relating private saving to the budget deficit and investment. The identity states that, in a closed economy, investment can be financed by a combination of private and public saving. In addition, changes in any of these three variables must necessarily affect at least one of the other two. However, the identity is silent about the determinants of changes in saving and investment, as well as the extent of their effect on other macroeconomic variables.

The IS curve

The IS curve represents combinations of income and the interest rate, such that the goods market is in equilibrium.

Analytically the IS curve is computed by replacing in the income identity (2.9) the behavioural equations for consumption, investment, tax revenue and government spending. The resulting equation has to be solved for the interest rate as a function of income, as the IS curve is always plotted in the income–interest rate space.

Before deriving the IS curve, I will simplify equations (2.3) and (2.4) by assuming that government spending is exogenous (g 1 = g 2 = 0) whereas taxes do not depend on consumption (τ 2 = 0).

i^* (1/b^2)(c_0 - c_1 barT + barI + barG) - (((1-c_1)(1-τ_1)-b)/(b^2))Y^*

In the above expression the symbols i* and Y* denote equilibrium values. Note we have used the assumption of fixed prices to replace the real interest rate r with the nominal rate i. The slope of the IS curve in absolute terms is negatively related to the marginal propensity to consume, c1 , the responsiveness of investment to output, b1 , and the interest rate, b2 ; it is positively related to the tax rate, τ1.

The larger the marginal propensity to consume, the flatter the IS curve, since a given increase in investment caused by a reduction in the interest rate, will then deliver a larger increase in income via the multiplier. Similarly, the more interest-sensitive investment spending is, the flatter is the IS curve, since a given reduction in the interest rate causes a relatively large increase in investment spending, which results in a larger increase in equilibrium income. An increase in b1 makes the IS curve flatter, since investment spending responds more to income for any given interest rate, and this amplifies the multiplier effect. Conversely, tax rate increases make the IS curve steeper as they dampen the multiplier effect of higher aggregate income on consumer expenditure.

The intercept of the IS curve depends upon the level of autonomous spending, c0 − c1 T + I + G . An increase (reduction) of autonomous spending shifts the IS curve upward (downward). Note also that the position of the IS curve is affected by the responsiveness of investment to the interest rate: the larger b 2 the smaller the intercept of the IS curve.

If the central bank controls the interest rate, the equilibrium level of income moves along the IS curve. An increase (decrease) in government spending raises aggregate demand, thus shifting upwards (downwards) the IS curve. The effect of changes in taxation depends upon the structure of the tax system. If taxes are levied as lump-sums, then tax changes can only change the position of the IS curve, without altering its slope.

However, if taxes are levied as a proportion of consumers’ income, any tax policy change has an effect on the slope of the IS curve.

The LM curve

The LM curve comprises combinations of the interest rate and income, for which the money market is in equilibrium.

Analytically, the LM curve is computed combining the equations for money demand (2.5) and supply (2.6). The resulting equation has to be solved for the interest rate as a function of income, since the LM curve is always plotted in the income-interest rate space. This yields the following

equation:

i^* = (1/h_2)(h_0 - (M/P) + (h_1/h_2) Y^*

The slope of the LM curve depends on the sensitivity of money demand to income and the interest rate, as measured by the coefficient h1 / h2 . The more money demand is sensitive to income, relative to the interest rate, the steeper the LM curve. If money demand does not respond to the interest rate, h2 = 0, the LM curve is vertical. A vertical LM curve is often referred to as the classical case. In contrast, if money demand is very sensitive to the interest rate, h2 = ∞ , the LM curve is horizontal. In this case it is not possible for the central bank to change the equilibrium interest rate through variations in the money supply. The case of a horizontal LM curve is often referred to as a liquidity trap.

Monetary policy affects the position of the LM curve. An expansionary monetary policy shifts the LM curve downwards, since it increases the liquidity in the money market and reduces the interest rate for any given level of income. In contrast, a contractionary monetary policy shifts the LM curve upwards, as it reduces the liquidity in the money market and increases the interest rate at any given level of income.

It may be useful to recall that, at this stage of the subject, the conduct of monetary policy is based upon the following simplifying assumptions:

1. The central bank has direct control over money supply through open market operations.

2. The government issues bonds on behalf of the central bank; the central bank does not directly issue bonds, but can only create money to buy bonds issued by the government.

3. Individuals are always willing to trade bonds at some price (i.e. bond demand from the private sector is unlimited).

To understand the link between monetary policy and money supply, you may find it convenient to consider the simplified central bank balance sheet in Table 2.1. The central bank’s assets are represented by bonds, while the central bank’s liabilities are represented by the currency (money) held by the public. To increase the money supply, the central bank has to purchase new bonds. This increases both assets (through the additional bonds) and liabilities (through the new currency created and exchanged for bonds). To reduce the money supply, the central bank sells bonds for existing currency. This operation reduces assets (through the sale of bonds) and liabilities (through the reduction of currency held by the general public).

| Central Bank | |

| Assets | Liabilities |

| Bonds | Money |

Table 2.1: Central bank balance sheet in a closed economy.

A more accurate description of the central bank’s balance sheet and the mechanism of money creation will be provided in Chapter 11 of the subject guide.

Equilibrium in the IS–LM model

The IS–LM model determines combinations of the interest rate and income that simultaneously satisfy the equilibrium condition in the goods market and in the money market. Analytically, the equilibrium level of output and the interest rate are computed by combining the IS equation in (2.11) with the LM equation in (2.12). For instance, if we replace the interest rate in the IS equation with the right-hand side of the LM equation, the equilibrium level of income is calculated as:

Note that the policy variables G and M both increase the equilibrium level of income. Tax policy affects Y* negatively through the term c1 T and the term c1 τ1 . Therefore, expansionary fiscal and monetary policies increase the equilibrium level of income. Conversely, fiscal and monetary contractions reduce the equilibrium level of income.

Alternatively, you can compute the equilibrium level of the interest rate by replacing the income level in the IS equation with the level of income from the LM equation. This yields the following expression for the equilibrium interest rate:

Fiscal expansions and monetary contractions increase the interest rate, whereas fiscal contractions and monetary expansions reduce the interest rate.

| Fiscal policy Expansionary | Fiscal policy Contractionary | Monetary policy Expansionary | Monetary policy Contractionary | |

| Output | + | - | + | - |

| Interest rate | + | - | - | + |

The table shows that the effect of fiscal policy, on output and the interest rate, is symmetric in the sense that an expansionary fiscal policy increases both output and the interest rate, while a contractionary fiscal policy reduces both variables. In contrast, monetary policy has an asymmetric effect on output and the interest rate: an expansionary monetary policy increases output while reducing the interest rate, whereas a contractionary monetary policy reduces output while increasing the interest rate.

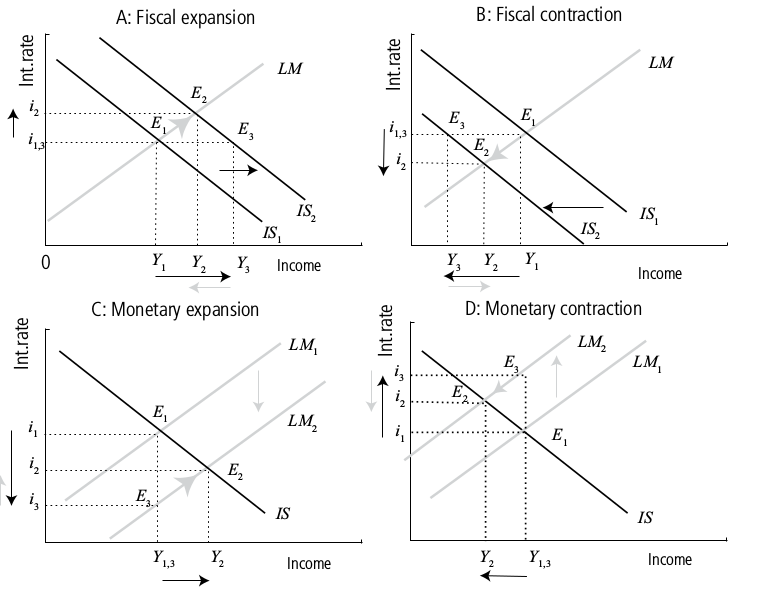

Fiscal and monetary policy in the IS–LM model

Figure 2.1 provides a graphical illustration of the effect of fiscal and monetary policy in the IS–LM model. In each panel, the initial equilibrium is the point E 1 , which corresponds to the level of income Y 1 and interest rate i 1 . Panel A shows that a fiscal expansion affects both the goods and the money market. In the goods market, the increase in aggregate demand resulting from the fiscal expansion raises the equilibrium level of income. Since the money supply is fixed, the increase in income increases money demand, which can only be accommodated by an increase in the interest rate. In turn, the increase in the interest rate causes a fall in investment spending (crowding out effect), which partially offsets the initial increase in income. The final equilibrium position is indicated in the graph by point E 2 , but, in general, depends upon the slope of the LM curve relative to the IS curve.

Conversely, Panel B shows that a fiscal contraction reduces the equilibrium levels of income and interest rate. Note that the fiscal contraction reduces aggregate demand and income in the goods market. The fall in income causes a contraction in money demand, and money market equilibrium is restored only by a fall in the interest rate. In turn, the fall in the interest rate stimulates investment spending and contributes to partially offsetting the initial reduction in income.

Panel C shows that a monetary expansion shifts the LM curve downwards. At the initial level of income, the interest rate drops from i 1 to i 3 , since the expansionary monetary policy operation raises the price of bonds and reduces the interest rate. The fall in the interest rate stimulates investment spending and increases output. Ultimately, the equilibrium converges to point E 2 . In general, the flatter the IS curve, the greater the monetary policy stimulus on output. Panel D shows how the IS–LM equilibrium adjusts as a result of a monetary contraction.

The effectiveness of monetary and fiscal policy – on the interest rate, income, and unemployment – crucially depends on the relative slopes of the IS and the LM curves. Broadly speaking, the flatter (steeper) the IS curve is, the more (less) effective is monetary policy on output and unemployment, relative to the interest rate. On the other hand, the flatter (steeper) the LM curve is, the more (less) effective is fiscal policy on output and unemployment relative to the interest rate.

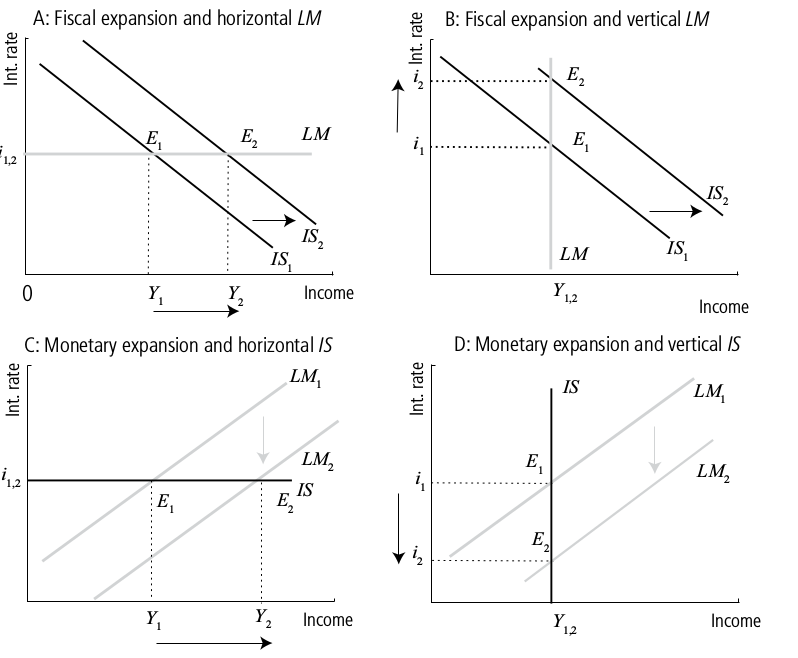

Figure 2.2 illustrates four extreme cases. A liquidity trap occurs when the public is prepared to hold any amount of money at the current interest rate. This implies that money demand is horizontal in the real money–interest rate space, and monetary policy is ineffective because changes in the money supply do not alter income and the interest rate. As a consequence, the LM curve is horizontal. If the economy is in a liquidity trap, fiscal policy is very effective, as there is no crowding out effect on investment following a fiscal expansion (Panel A). The classical case occurs when money demand is entirely unresponsive to the interest rate, so that the LM curve is vertical (Panel B). This is consistent with the classical quantity theory of money, which states that nominal income, PY, is entirely determined by the money supply. In this case, if we assume that the price level is fixed then a monetary expansion has a one-to-one effect on real income, whereas fiscal policy has no effect on income because the fiscal expansion causes the interest rate to rise, reducing investment spending one-for-one with the rise in government spending. 9

The effectiveness of monetary policy depends upon the slope of the IS curve. If investment is fully sensitive to the interest rate, then the IS curve is horizontal. This implies that an expansionary monetary policy will exert all its effect (Panel C). Vice versa, if investment is completely insensitive to the interest rate the IS curve is vertical, which implies monetary policy ineffectiveness (Panel D).

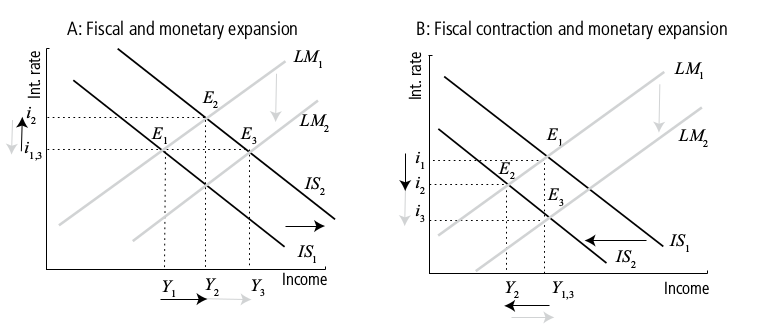

Policy mixes

The IS–LM model shows that fiscal and monetary policies can be used either in isolation, or simultaneously, to influence key macroeconomic variables, such as the real interest rate and output. Since output and employment are positively correlated, that is employment increases (decreases) when output increases (decreases), fiscal and monetary policy also influence the unemployment rate.

It is important that you know how to employ the IS–LM model to prescribe the appropriate policy mix to achieve a specific macroeconomic outcome. For instance, if the government and the central bank plan to increase output, without changing the interest rate, this goal can be achieved through a combination of expansionary fiscal policy and expansionary monetary policy. The expansionary fiscal policy increases both output and the interest rate, while the expansionary monetary policy increases output, but reduces the interest rate (Figure 2.3, Panel A). Another example occurs when policy-makers want to reduce the interest rate, while keeping the level of output unaffected. This goal can be achieved through a combination of expansionary monetary policy, which reduces the interest rate and increases output, and a contractionary fiscal policy, which will further contribute to the reduction in the interest rate while reducing output (Figure 2.3, Panel B).

Blanchard, O., Macroeconomics (Fifth Edition), Pearson International Edition, 2009.

Chapter 3

Production = Sales + Inventory; Inventory = Production - Sales; Sales = Production - Inventory

Total demand for goods Z := C + I + G + X - IM

C_0 is what you must spend (even if income is 0). C_1 is marginal propensity to consume. Consumption function, y axis = Consumption, x axis = disposable income, C_0 is starting point on y at x = 0, C_1 is upward slope, less than 45 deg (usually?) C = c_0 + c_1 Y_D (disposable income). Y_D = Y-T

Equibrium in the goods market sugggests that production equals demand. Demand depends on income which is equal to production.

Y = C + I + G; Y - T - C = I + G - T; Y - T - C = S = I + G - T; I = S + (T - G)

Chapter 4

Simplify money that pays not interest; bonds as all interest-bearing accounts.

A low interest rate increases the demand for money. An increase in nominal income increases interest rate (M^S is vertical M^D downward sloping, y-axis interest, x-axis money demand)

Chapter 5

Fiscal Policy Shift of IS Shift in LM Output Interest Rate

Increase Taxes Left None Down Down

Decrease Taxes Right None Up Up

Increase Spending Right None Up Up

Decrease Spending Left None Down Down

Increase Money None Down Up Down

Decrease Money None Up Down Up

Dornbusch R., Fischer, S., Startz, R., Macroeconomics (9th edition, international), McGraw-Hill, 2004

Chapter 9

Aggregate demand is the total amount of good demanded in the economy: AD = C + I + G + NX

Output is at an equilibrium when the quantity produced is equal to the amount demanded: Y = AD = C + I + G + NX

The equilibrium level of output is higher the larger the marginal propensity to consume, c, and the higher the level of autonomous spending barA (or c_1, c_0 in Mankiw)

Chapter 10

The IS-LM model finds the values of GDP and the interedst rate which simultaneously clear the goods and money markets.

The IS curve (or schedule) show combinations of interest rates and levels of output such that planned spending equals income.

The smaller the sensitivity of investment spending to the interest rate the smalleer the multiplier, the steeper the IS curve.

The LM curve (or schedule) show combinations of interest rates and levels of output such that money demand equals money supply.

The greater the responsiveness of the demand for money to income the lower the responsiveness or the demand for money to the interest rate, the steeper the LM curve will be.

Chapter 11

When the LM curve is vertical monetary policy has a maximal effect on the level of income, and fiscal policy has no effect on income.

Crowding out occurs when expansionary fiscal policy causes interest rates to rise, thereby reducing private spending, particularly investment.

| Interest Rate | Consumption | Investment | GDP | |

| Income Tax Cut | + | + | - | + |

| Government Spending | + | + | -+ | |

| Investment Subsidy | + | + | ++ |

Real interest rate is nominal rate minus inflation

Mankiw N.G., Taylor M.P., Macroeconomics (European Edition), Worth, 2008

Chapter 9

"*In the long run, prices are flexible and can respond to changes in supply and demand. In the short run, many prices are 'sticky' at some predetermined level*". p276

In classic macroeconomic theory output depends on the ability to supply, which depends on capital and labour. When prices are sticky output also depends on demand. Hence a model of aggregate supply and aggregate demand. p278.

"**Aggregate demand** (AD) is the relationship between the quantity of output demanded and tha aggregate price level" p278

AD slopes downward, Y-axis P (price level), X-axis income, output Y. High price, low demand/output, low price, high demand/output. Reduction in money supply moves aggregate demand to the left, increase moves to the right.

MV = PY (money supply, M; V velocity of money; P price level, Y is output). Also;

M/P = (M/P)^d = kY, where KY = 1/v, a parameter determining how much money people want to hold for every euro of income, supply of real money balances M/P equats the deamnd for real money balances (M/P)^d

"**Aggregate Supply** (AS) is the relationshiup between the quantity of goods and services supplied and the price level" p281.

AS slopes upward, Y- axis P (price level), X-axis output Y. Differentiate between Long-Run Aggregate Supply (LRAS) and Short-Run Aggregate Supply (SRAS).

In LRAS firms can change prices to adapt, but in SRAS prices are sticky. LRAS curve is vertical, barY; output is measured by Kapital and Labour (K&L). A fall in AD will lower the price in LRAS, but the output will remain the same.

In SRAS firms cannot change prices immediately; SRAS curve is horizontal. Regardless of changes in demand, price remains the same. A fall in AD still results in the same price P.

The long-run equilibrium is where LRAS, SRAS, and AD intersect.

A shift to the AD is called a demand shock, a shift to AS is called a supply shock. Stablisation policy aims to minimuse the severity of short-run fluctuations.

e.g., readily available credit cards reduces money demand with an equivalent increase in money velocity (1/k). Spending rises and a there's an economic boom. Over time, pulls up wages and prices. A stablisation policy to offset the increase in velocity would be to reduce money supply. An adverse supply shock (e.g., destruction of crops) or a favourable price shock (e.g., break up of an oil cartel). Adverse cause SRAS to shift upwards, increasing prices and demand falls (stagflation, increasing prices, falling output). Stablisation will be by raising aggregate demand, which stablises output but at a higher price level.

When GDP declines so does consumption (by a smaller amount) and investment (by a larger amount), and unemployment rises.

Chapter 10

Two parts of IS-LM are investment-saving and liquidity-money. Interest rate influences both and links the two variables.

Keynesian Cross: Actual expenditure versus desired Planned expenditure.

In a closed economy E = C + I + G (planned expenditure = consumption plus investment, government expenditure). Assume fixed I and G and fixed taxes, becomes E = C(Y-barT) + barI + barG.

Planned expenditure depends on income, because higher income leads to higher consumption.

The economy is in equilibrium when planned expenditure = actual expenditure, E = Y, 45 deg on the Keynesian cross, E = planned expenditure, y axis, Y equals income, output X axis. Planned starts higher but has lower gradiant. Too much Y (actual) over E (planned) means inventory accumulation, incomes fall, too much E (planned) over Y (actual) means inventory declines, incomes rise.

A change in G causes a greater change in Y; deltaY/deltaG > 1. Higher income means high econsumption, which raises income, which raises consumption etc. How much? Depends on Marginal Propensity to Consume (MPC).

deltaY/deltaG = 1/(1-MPC) (limit on geometric series)

Likewise a decrease in taxes will have the same effect (a "tax multiplier"). A decrease in taxes raises effective income and output which leads to an increase in interest rates.

Fiscal policy, however, is also sticky! Government expenditure takes time, tax cuts take time etc. Interest rates to the rescue! An increase in interest rates reduces investment which shifts planned expenditure downward, and a fall in income and output.

The IS Curve is derived from the downward sloping investment Curve and the Keynesian Cross.

A loanable funs interpretation of the IS Curve: Y - C -G = I; S = I. Y - C(Y-T) - G = I(r)

An increase in income raises saving causing interest rates to drop.

Liquidity Preference: In the short-run the interest rate adjusts to balance the supply and demand for the economy's most liquid asset - money. Keynesian cross builds the IS curve, liquidity preference the LM curve.

Assume fixed supply of real money balances (M/P)^s = barM/baP; Money supply is exogenuous variable chosen by the central bank. Supply (barM/barP) is fixed. Demand, downward slopin L(r). Y axis interest rate, r, x axis real money balances M/P. High interest rate, low M/P, low interest rate, high M/P. Shift right change in barM/barP (expansion) will increase real money balances, reduce interest rates, shift left (contract) will reduce, increase interest rates.

When income is high, expenditure is high, more transactions, greater money demand; (M/P)^d = L(r,Y). The quanity of real money balances is negatively related to the interest rate and positively to inocme.

An increase in income raises money demand an increases interest rate which is derived to the upward sloping LM curve. A reduction in money supply shifts the LM curve upward, increasing interest rates.

The whole equation:

Y = C(Y-T) + I(r) + G is IS downward sloping, interest r (Y axis), income, output Y (x axis)

M/P = L(r, Y) is LM is upward sloping.

Keynesian Cross leads to IS Curve. Liquidity Preference leads to LM Curve. Combined, leads to IS-LM. IS-LM model leads to Aggregate Demand

Aggregate Demand (AD) and Aggregate Supply (AS) leads to ASAD, whoich provides explanation of short-term fluctuations.

Chapter 11

"*an increase in the money supply lowers the interest rate which stimulates investment and thereby expands the demand for goods and services"* p323-324

A tax increase shifts IS left with no change in money supply means lower income and lower interest rates

A tax increase shifts IS left with reduced money supply shifts LM left means even lower income but no change to interest rates

A tax increase shifts IS left with expanded money supply shifts LM right means no change to income but even lower interest rates.

From IS-LM to AD.

An increase in price level shifts LM upward, lowering Y with IS stable. This is reflected in the AD curve, an increase in P is a reduction in Y. Likewise a monetary expansion in LM increases Y wheras a fiscal expansion shifts IS right, increasing Y and r,