Chapter 4: Inflation and the Phillips curve

Aims of the chapter

This chapter focuses on the links between output and inflation in the long run and over the business cycle. We revise the Phillips curve and how economists’ view of the inflation–unemployment trade-off has changed over time. Next, we exploit the link between the Phillips curve and the SRAS to revisit the AD–AS model in output-inflation space. This yields a complete new model of inflation, which is employed to assess the likely impact of disinflation policies under alternative assumptions about the mechanism of expectations formation.

• illustrate the derivation of the Phillips curve and discuss its alternative interpretations

• describe the links between the Phillips curve, Okun’s law, and the SRAS relation

• employ the AD–AS model in output-inflation space to describe the behaviour of the economic system in the long run and over the business cycle

• list and discuss the different costs and benefits of inflation

• illustrate the quantity theory of money, and its long-run implications for monetary policy

• discuss the relevance of the Lucas critique, and the role of rational expectations within disinflation policy

• describe the short- and long-run implications for macroeconomic policy of inflation expectations.

This chapter covers the section of the syllabus on the determination of the inflation rate and the assessment of disinflation policy. It begins by revising the definition of the inflation rate and the alternative versions of the Phillips curve. It is very important that you have a good understanding of the empirical evidence on the inflation-unemployment trade-off before and after the 1970s, and that you can relate the changes in the empirical evidence to the alternative analytical formulations of the Phillips curve.

We focus on the link between the Phillips curve and the SRAS relation, and show how they are related through the so-called Okun’s law. This allows us to revisit the AD–AS model within output-inflation space. The new framework provides a more plausible description of the economy over the business cycle, as it predicts that economies during downturns should go through a phase of disinflation, rather than deflation as predicted by the basic AD–AS model developed in the previous chapter. Throughout the discussion, we emphasise that business-cycle fluctuations are automatically dampened by movements in the inflation rate, and that the effectiveness of the adjustment mechanism, in turn, increases with the degree of price flexibility. We have also seen, in the previous chapter, how monetary and fiscal policy can be employed to further reduce economic fluctuations and to speed up the adjustment mechanism.

The inflation model developed in this chapter is then employed to analyse the role and the effectiveness of a disinflation policy. We revise three alternative views of the model. The traditional view is based upon the assumption that the mechanism adopted by the private sector to form inflation expectations is backward looking (adaptive expectations). In this case, disinflation can only be achieved at the cost of high unemployment in the short run. We explain how the traditional approach was challenged by the famous ‘Lucas critique’, which argued against the use of backward-looking models to predict the likely effects of policy changes. The second model of disinflation is based upon Lucas’s view that if the private sector has rational expectations then disinflation can be achieved at zero cost, provided that monetary authorities are credible. Finally, we discuss the Fischer–Taylor view of disinflation policy in the presence of nominal rigidities, which shows that disinflations could be costly even with credible monetary authorities.

The chapter concludes by focusing on situations which can explain persistence in business-cycle fluctuations, by considering the role played by inflation expectations during recessions, and when economies are in liquidity traps.

It is essential to understand the difference between the level and the growth rate of a variable, and, in the specific case of this chapter, the different roles played by the price level and the inflation rate. The level of a variable indicates the value that it takes in a specific period of time. The growth rate indicates the speed

at which the level changes over time. Inflation is defined as a persistent increase in the price level (i.e. a positive growth rate of prices). Note also that an assumption that expected inflation equals lagged inflation is not

equivalent to an assumption that the expected price level equals the price level. The two only coincide if the lagged inflation rate is zero.

The inflation rate and the Phillips curve

The relationship between inflation and unemployment is known as the Phillips curve. It follows from the AS relationship that we studied in the previous chapter. As we saw there, there are at least four different ways to understand aggregate supply. Here we focus on the WS–PS approach, an advanced version of the Worker Misperception Model, starting with the equation:

P_t = P_t^e (1+μ)(1 + z – αu_t ).

One can derive from the above expression the following (approximate) expression for the inflation rate:

pi_t = pi_te + (μ + z) – αu_t , (4.1)

which can alternatively be written as:

pi_t = pi_t^e – α(u_t – u_n ),

where pi_t is the actual inflation rate in period t, pi_t^e is the expected inflation rate in period t, and we have used the approximation from (3.7): αu_n ≅ μ + z. The solution to equation (4.1) depends upon the mechanism by which expectations are formed. In the special case of adaptive expectations, inflation is forecast according to an autoregressive equation, pi_t^e = θpi_t−1 for some parameter θ, and the inflation rate becomes:

pi_t = θpi_t−1 − α( u_t − u_n ), (4.2)

which shows that the current period rate of inflation is a function of the previous period rate of inflation as well as the deviation of unemployment from its natural rate. Equations (4.1) or (4.2) give two functional forms for the determinants of the inflation rate, and changes any of the parameters of the two expressions affect the inflation rate.

The Phillips curve was first discovered by Alban William Phillips in 1958. Phillips observed an inverse empirical relationship between the annual rate of inflation and the annual unemployment rate in the United Kingdom from 1861 to 1957. The same negative relationship was found by Robert Solow and Paul Samuelson in the US using data from 1900 to 1960. The inflation–unemployment trade-off also held throughout the 1960s, with the constant decline of the unemployment rate in that period being associated with a steady rise in the rate of inflation.

It is essential that you are aware of the differences between the original and the modern Phillips curves, as well as the reasons behind the breakdown of the Phillips curve which occurred at the end of the 1960s. The original Phillips curve is analytically obtained by setting π et = 0 in equation (4.1) or, alternatively, θ = 0 in equation (4.2). This yields the expression:

pi_t = ( μ + z ) − αu_t , (4.3)

which suggests that there is a linear relationship between unemployment and inflation, with negative slope equal to α and intercept given by μ + z. The coefficient a measures the extent of the trade-off between unemployment and inflation and has a very important policy interpretation: a macroeconomic policy that reduces the unemployment rate by 1 per cent increases inflation by α per cent. Conversely, a policy aiming at reducing inflation by 1 per cent results in an increase in unemployment of 1/α per cent.

The modern Phillips curve allows instead for the expected inflation rate to be different from zero. It is obtained by rewriting equation (4.1) as:

pi_t − pi_t^e = − α( u_t − u_n ) , (4.4)

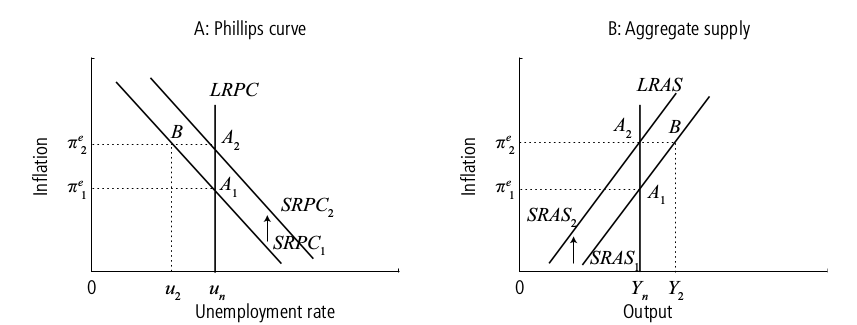

which shows that the current inflation rate depends upon the expected inflation rate and the deviation of unemployment from its natural rate. Under adaptive expectations, expected inflation is proportional to past inflation, and the Phillips curve is analytically described by equation (4.2). Figure 4.1 gives a graphical analysis of the properties of the Phillips curve in equation (4.4). Panel A shows that the curve is downward-sloping in unemployment-inflation space, and that expected inflation is constant along the Phillips curve at the rate π e , which occurs when u_t = u_n . Panel B shows that, given the natural unemployment rate, any increase in expected inflation shifts the Phillips curve upwards, one-for-one. Panel C shows the effect of an economic expansion on the Phillips curve. The economy starts from the equilibrium position A^1 . After the expansion the unemployment rate falls below the natural rate, u_1 < u_n , and the economy moves to point B along the original Phillips curve, PC_1 .

At point B actual inflation exceeds expected inflation, π_2 > π_1e . As a result, inflation expectations increase. For the case illustrated, the new level of inflation expectations is π e 2 = π 2 , corresponding to the curve PC_2 . Long-run equilibrium is now possible only at the point A 2 , with a higher rate of inflation than originally and unemployment back at the natural rate. Therefore, the modern Phillips curve predicts that after an economic expansion, inflation and the unemployment rate both increase as the economy returns to the natural unemployment rate. Conversely, panel D shows that as a result of an economic recession unemployment is higher than the natural rate and expected inflation falls, which leads the Phillips curve to shift downwards. While the economy recovers from a recession both inflation and the unemployment rate decrease, until unemployment returns to its natural rate. From a policy perspective, equation (4.4) implies that the attempt of policy makers to maintain the unemployment rate permanently below the natural rate leads to ever-increasing inflation, since expected inflation will continue to rise, and the Phillips curve will continue to shift upwards. Consequently, macroeconomic polices aimed at keeping output permanently above its natural level are ultimately unsustainable because they yield an ever-increasing inflation rate. Furthermore, panel C in Figure 4.1 helps to explain the empirical breakdown of the original Phillips

curve during the 1970s. Throughout that period, continuous changes in inflation expectations caused the Phillips curve to shift over time, so that econometricians were, ultimately, collecting inflation and unemployment rate observations from different Phillips curves. Therefore the 1970s data could not display the stable inflation–unemployment trade-off observed until the 1960s.

Okun’s law

Okun’s law is the name given to the relationship between changes in the unemployment rate and percentage changes in aggregate output.

Okun’s relation can be written as:

Y_t − Y_n/Yn = − γ( u_t − u_n ),

which posits that if unemployment is one percentage point higher than its natural level, then aggregate output is γ per cent lower than its natural level.

The above can be equivalently written as:

Y_t − Y_n = − δ ( u_t − u_n ) (4.5)

where the coefficient δ = γY_n measures how deviations of unemployment from the natural rate affect the output gap.

In general, since it relates output and unemployment, Okun’s law translates the upwards-sloping SRAS curve into the downwards-sloping Phillips curve in equation (4.4), or vice versa. Since Okun’s law in equation (4.5) implies that:

u_t − u_n = −(1/δ)(Y_t - Y_n)

the SRAS relation can be written as:

pi_t - pi_t^e = (α/δ) - (Y_t - Y_n)

or equivalently:

pi_t - pi_t^e = λ( Y_t − Y_n )

which shows that Okun’s law ultimately relates the slope of the SRAS and the Phillips curves. Consequently, it is easy to distinguish the short-run Phillips curve (SRPC), which is negatively sloped and described by equation (4.4), from the long run Phillips curve (LRPC), which is vertical in inflation-unemployment space at u_t = u_n.

Figure 4.2 gives a graphical representation of the relation between the Phillips curve and aggregate supply. Panel B shows that for a given level of expected inflation, pi_1^e , output can exceed its natural level (Y_2 > Y_n )

only temporarily, since in the long run the SRAS curve shifts upwards, from SRAS_1 to SRAS_2 . Correspondingly, panel A shows that the inflation–unemployment trade-off can only be temporary. Attempts to sustain an unemployment rate below the natural level, u_2 < u_n , lead to increased inflation in the short run. In the long run actual inflation settles at the higher expected rate, as the short-run Phillips curve shifts upwards from

SRPC_1 to SRPC_2 . Therefore, there is no inflation-unemployment trade off in the long run.

The theoretical version of Okun’s law, derived in equation (4.5), is slightly different from the empirical version sometimes taken to data, given by:

u_t − u_t − 1 = − β ( g_Yt − g_Yn ) (4.6)

where g_Yt and g_Yn are growth rates of actual and natural output.

This version of Okun’s law states that changes in the unemployment rate over a specific period of time depend upon the difference between the actual and the natural growth rate of output. The unemployment rate is unchanged if

output grows at the natural rate. The focus of the empirical analysis is on estimating β. In the USA, the empirical estimates, based on annual data, suggest that β = 0.4, (i.e. a one percentage point fall in the unemployment

rate is approximately associated with a 2.5 per cent increase in output). However, this result is not constant across countries and over time. For instance, over the period 1960–1980 the estimated β was about 0.15 in

the United Kingdom, and 0.02 in Japan, whereas in the subsequent period 1980–2003 the estimated β increased to 0.54 in the United Kingdom, and to 0.12 in Japan

The magnitude of β depends on how firms adjust their labour demand in response to production fluctuations, which in turn is affected by the degree of job security and labour market regulation. In principle, low estimates of β are associated with high levels of job security. Therefore the increase in the values of β estimated in the United Kingdom and Japan could be explained by labour market reforms aimed at weakening the legal restrictions on hiring and firing, undertaken in both of these two countries since the early 1980s.

The AD–AS model (revisited): long run

The aggregate demand relation was derived in equation (3.12) of the previous chapter, and it is rewritten in a more compact form below as:

Y = B + φ (M/P)

where the coefficient

B = ((h_2 b_2)/(h_1b_2)+(h_2m))[(1/b^2)A - (h_0/h_2)]

captures the effects of fiscal policy and private sector shocks on the position of the AD curve, and the parameter

φ = b_2/(h_1 b_2 + h_2 m )

measures the response of aggregate demand to changes in nominal money and the price level or, equivalently, changes in the real money supply.

Suppose for simplicity that B ≅ 0 holds. Then we can take logorithms of both sides of the AD relationship for periods t–1 and t, to obtain:

ln Y_t − ln Y_t−1 = ln M_t − ln M_t − 1 − ( ln P_t − ln P_t − 1 )

which is equivalent to:

g_Yt = g_Mt − pi_t

This equation expresses aggregate demand in terms of growth rates showing that the growth rate of real output, g_Yt , is equal to the difference between the growth rate of the nominal money supply, g_Mt , and the inflation rate, pi_ t . As a result, real output grows to the extent that growth in the nominal money supply exceeds inflation, g_Mt – pi_t > 0, or, equivalently, to the extent that the real money supply grows.

We can now employ the Phillips curve of equation (4.4), the empirical Okun’s law of equation (4.5), and the aggregate demand relationship in (4.7), to provide a full and new description of the behaviour of the economy in the long run and over the business cycle.

In the long run, the following propositions are true:

1. By definition, the unemployment rate is constant and equal to the natural rate: u_t = u_n .

2. The growth rate of output is constant and equal to the natural rate: g_y = g_yn

3. The inflation rate is entirely determined by the growth rate of the nominal money supply. Aggregate demand implies that: π_t = g_M − g_Yn, where g_y is a constant.

4. The inflation rate is constant only if the central bank maintains a constant growth rate of the nominal money supply, g_Mt = g_M : pi_t = pi_t − 1 = barpi = g_m - g_yn

5. A constant inflation rate is consistent with the unemployment rate being equal to the natural rate, and actual inflation being equal to expected inflation. In fact, the Phillips curve shows that:

pi_t = pi_t-1 = barpi = pi^e => u_t = u_n

This analysis implies that in the long run inflation is entirely determined by monetary policy. The natural rate of unemployment and the natural level of output are determined by equilibrium in the labour market. In other words, money is neutral in the long run, in the sense that nominal money growth has no long-run effect on real variables, such as output, investment and unemployment.

The AD–AS model (revisited): short run

The behaviour of the economy over the business cycle is described in Figure 4.3. Panel A considers the adjustment mechanism after an economic expansion. Suppose the initial equilibrium is at point A 1 : output is at the natural level Y n , the rate of nominal money growth equals the inflation rate, actual inflation equals expected inflation, π 1 = π 1 e , and the equilibrium interest rate, in the IS–LM diagram, equals i 1 Suppose, next, that the economy is hit by a positive demand shock, caused for example by an expansionary monetary policy. As a result, the LM curve shifts downwards and the interest rate reduces to i 1 ' , output increases to Y 1 ', and the short run equilibrium moves to A 1 ' on the SRAS 1 . 6 Okun’s law implies that the increase in output causes the unemployment rate to fall below the natural rate. From the Phillips curve it follows that inflation begins to increase. The demand equation in (4.7) shows that the increase in inflation reduces real money growth, which shifts the LM curve upwards until the natural level of output is restored.

Contemporaneously, also the Phillips curve and the SRAS shift upwards until the economy returns to its long-run equilibrium position at point A 2 , where expected inflation is in line with the higher inflation rate π 2 = π 2 e . Panel B shows the adjustment of the economy to a negative shock, caused by a monetary contraction. The economy starts from an equilibrium position at A 1 , at which output is at its natural level. Next, the demand shock reduces output below its natural level and unemployment increases above the natural rate. The short run equilibrium in the economy shifts to point A 1 ' along the initial SRAS (Phillips) curve. 7 The Phillips curve predicts that inflation will begin to decline, and this increases the growth rate of the real money stock. The increase in the growth rate of real money shifts the LM curve downwards until the natural level of output is restored. Contemporaneously, inflation declines as the SRAS (Phillips) curve shifts downwards to point A 2 , where the expected inflation rate equals the lower inflation rate π 2 = π 2 e .

There is an essential point that needs to be clarified at this stage. Even though, from a graphical point of view, the adjustment mechanism in the revised AD–AS model looks similar to that described in the previous chapter of the subject guide, the two mechanisms are conceptually very different. In the basic AD–AS model developed in the previous chapter, with no inflation and a fixed money supply, an adverse shock drives output below its natural level and causes a decline in the price level, which in turn increases the real money supply. The increase in the real money supply shifts the LM curve to the right until the natural level of output is restored. Therefore, this adjustment mechanism implies that while the economy recovers from a recession the price level decreases

(i.e. the economy experiences a deflation). The problem with this type of adjustment mechanism is that deflation is seldom observed in the real world. In contrast, the adjustment mechanism developed in this chapter

exploits the Phillips curve in equation (4.4), which implies that during recoveries from recession economies experience disinflation (i.e. a decrease in inflation, which is a hypothesis consistent with the empirical

evidence).

Costs and benefits of inflation

Economists normally distinguish between the costs of expected inflation and the costs of unexpected inflation. Expected inflation is an increase in price level that is perfectly anticipated by the private sector and is,

therefore, taken into account in economic transactions. The costs arising from anticipated inflation are ‘shoe-leather’ costs, menu costs, changes in relative prices, and tax distortions. When inflation rises, the nominal

interest rate increases, thus increasing the cost of holding money. For this reason people want to hold less money and make more trips to banks in order to withdraw small quantities of cash. The cost of these trips is normally referred to as shoe-leather costs. Menu costs are the costs of updating catalogues, vending machines, cash registers, etc., due to the general increase in the price level. If the price of some goods increases more than others, then inflation changes relative prices of goods, thus altering consumption patterns. If price increases between different goods are staggered, so that the price of one may increase some months after another in response to the same general inflationary trend, then relative prices in the economy are likely to be constantly changing, and this can be a source of inefficient resource allocation. Finally, inflation causes tax distortions to the extent that the tax system is not perfectly indexed. The rise in inflation may increase taxpayers’ nominal incomes. If tax brackets are not updated to take into account inflation, some people are taxed more as a result only of a nominal, rather than a real, increase in income.

Unexpected inflation refers to unanticipated future increases in the price level, which are not taken into account in economic transactions. The main costs arising from unanticipated inflation are due to the redistribution of wealth between debtors and creditors. Wealth redistributions arise because inflation erodes the real value of assets and liabilities fixed in nominal terms, such as money, long-term bonds, fixed-term mortgages, saving accounts, insurance contracts, and fixed pensions. Unanticipated inflation implies that debtors (mortgage holders or bond issuers) pay less than expected in real terms, and creditors (mortgage issuers or bond holders) receive less than initially anticipated. For this reason, the higher the inflation variability is, the higher the price uncertainty faced by creditors and debtors, and the more likely are these unexpected wealth redistributions. Moreover, the empirical evidence suggests that high inflation rates are often associated with higher inflation volatility, which increases the likelihood of unexpected, and potentially large, wealth redistributions. Of course, wealth redistributions are not a ‘cost’ for everybody: debtors are likely to welcome unexpected inflation as it increases their net wealth.

Although this discussion might suggest that the ideal inflation rate should be zero, most economists believe that the optimal rate is instead positive, though low. This is because a low inflation rate brings at least three types

of benefits to an economy. First, inflation brings positive revenue to the government through the printing of money – seignorage – which can be used either to lower the budget deficit or to decrease other taxes. The seignorage income is, however, quantitatively very low unless the inflation rate is very high. Second, a positive rate of inflation allows central banks to achieve low if not negative real interest rates, which could help the recovery from an economic recession. Finally, positive actual and expected inflation allows firms to cut real wages without reducing nominal wages, by ensuring that workers’ nominal wages increase less than the inflation rate (money illusion).

Costly disinflation policy

The Phillips curve in equation (4.2) suggests that in order to reduce the inflation rate an economy must go through a period of low output and high unemployment. Panel B in Figure 4.3 shows that if the central bank wants to reduce the inflation from a high rate pi_1 to a lower rate pi_2 , this can only be achieved at the cost of an economic recession, Y'1 < Yn . In other words, the model suggests that disinflation is costly: any policy aimed at reducing the inflation rate in the medium run comes at the cost of higher unemployment in the short run. The sacrifice ratio is a measure of the cost of disinflation policy. It computes the cumulative loss in employment required to achieve a given reduction in the price level, measured as a proportion of the achieved reduction in inflation.

Analytically, the sacrifice ratio, SR, is written as:

SR = ((u_t - u_n)/(pi_t - pi_t-1)) = -((u_t - u_n)/(∆pi_t))

For example, suppose that the Phillips curve in equation (4.2) is estimated to be given by:

pi_t - pi_t-1 = -(1/2)(u_t - u_n)

where the time subscript t indicates end-of-year observations. Therefore, the estimated Phillips curve suggests that a 1 per cent annual reduction in inflation, pi_t - pi_t-1 = -1, requires a 2 per cent short-run loss in terms of

unemployment, u_t - u_n = 2. In other words, the sacrifice ratio implied by the estimated Phillips curve is equal to:

SR = -((u_t - u_n)/(∆pi_t)) = 2/-1 = 2

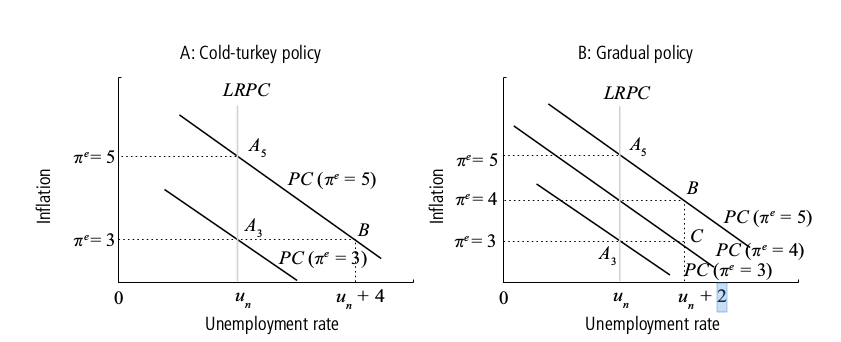

The total cost of a disinflation policy can be measured by multiplying the sacrifice ratio by the number of percentage points by which the central bank wishes to reduce inflation. For instance, if the sacrifice ratio is 2, then reducing inflation by 5 percentage points requires a cumulative increase in the unemployment rate 10 percentage points above the natural rate. Although policy-makers cannot affect the overall cost of disinflation policy, which is ultimately determined by the slope of the Phillips curve, they have control over the length of the resulting recession, which ultimately depends upon how quickly the central bank wants to reduce inflation.

This is illustrated in Figure 4.4, which considers an economy in which the central bank wants to reduce the inflation rate from 5 to 3 per cent, assuming a sacrifice ratio of 2. Panel A shows that if the central bank wants to achieve the lower inflation target in one year, then the economy has to go through a one year deep recession (point B) with unemployment 4 per cent higher than the natural level. Alternatively, panel B shows that if the central bank wants to adopt a more gradual approach and reduce inflation by one percentage point per year (points B and C), the economy will go through a two-year recession, with unemployment 2 per cent higher than the natural level each year.

Ultimately, the speed of the adjustment and the length of the recession depend upon central bank preferences. Note also that the linearity of the Phillips curve implies that the sacrifice ratio for reducing inflation, from 5 to 3 per cent, is independent of the speed of the adjustment. As a result, a cold-turkey or shock therapy policy, which consists of rapidly reducing the rate of inflation to the new low level, yields the same sacrifice ratio of a more gradual policy, which entails a longer period of disinflation. This result does not hold if the Phillips curve is non-linear. The empirical evidence suggests that the Phillips curve may be convex, which implies that the inflation-unemployment trade-off changes with the unemployment rate and, in particular, that inflation becomes less sensitive to changes in unemployment the higher the unemployment rate.

Disinflation policy

In the mid-1970s, the economist Robert Lucas challenged the traditional view that inflation could only be reduced at the cost of higher unemployment and that the speed of the deflation had no effect on the sacrifice ratio. Lucas first argued that the use of a model such as the AD–AS with adaptive expectations to predict the consequences of a disinflation policy is bound to provide misleading forecasts, since the estimated Phillips curve and Okun’s law

depend on historical data, and policy changes are likely to alter the observed relationships between variables. In particular, policy changes may alter both the response of unemployment to output, and inflation expectations, thus

changing both the slope and the position of the Phillips curve. This argument is known as the Lucas critique.

Lucas went on to argue that a disinflation policy could be costless, if monetary authorities are credible and people have rational expectations. In the Phillips curve of equation (4.2) expected inflation is based on lagged inflation. Consequently, disinflation automatically leads to short-run high unemployment. However, rational expectations do not consider past inflation, but are formed according to the best predictions that the private sector could make about the future evolution of the price level given the information available about the state of the economy and economic policy. The Phillips curve in equation (4.4) suggests that if the central bank could convince wage setters that it intended to reduce inflation in the future, wage setters might expect inflation to be lower in the future than in the past. If the central bank announces a lower inflation target, and wage setters find it credible, disinflation could be achieved without any short-run increase in the unemployment rate. In other words, the sacrifice ratio is zero when monetary authorities are credible, and the policy prescription arising from Lucas’ view is that central banks can and should pursue fast disinflation policies. Analytically, the Lucas argument is illustrated by combining the Phillips curve in equation (4.4),

pi_t − pi_t^e = − α (u_t − u_n )

with expectations given by:

pi_t^e = bar pi.

where bar pi is the inflation target announced by the central bank. Therefore, if the inflation target is credible, the Phillips curve is described by:

pi_t - bar pi = α (U_t − U_n)

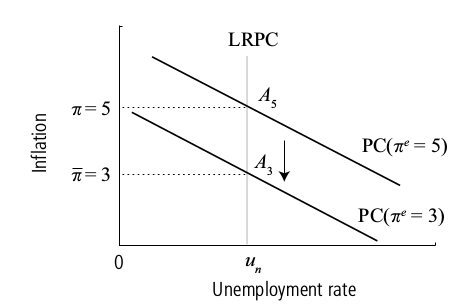

This suggests that monetary authorities can have full control over the position of the Phillips curve, provided that (i) their policy actions (and announcements) are credible and (ii) people incorporate the target inflation rate into their expectations. Figure 4.5 gives a graphical illustration of costless disinflation policy by considering an economy in which, as in Figure 4.4, the central bank wants to reduce the inflation rate from 5 to 3 per cent. If monetary policy is credible, once the central bank announces the new lower inflation target, the Phillips curve immediately shifts downwards and the economy adjusts to the new equilibrium at A 3 , in which actual inflation equals the lower 3 per cent target.

In contrast to the Lucas argument, Stanley Fischer and John Taylor have argued that the presence of nominal rigidities implies that even credible disinflations could be costly. Fischer emphasised that inflation is already built into existing wage agreements and cannot be reduced without cost. Taylor pointed out that wages are not all set simultaneously, but instead are staggered over time. The existence of staggered contracts implies that wages (and hence prices) can adjust only slowly to changes in policy. As a result, a too-rapid reduction in nominal money growth would lead to a less than proportional decrease in inflation. The consequent decline in the real money stock would lead to a recession and an increase in the unemployment rate. The policy prescription arising from the nominal

rigidities view is that the central bank should implement disinflation policies slowly.

Analytically, the Fischer–Taylor view implies that the inflation target announced by the central bank affects inflation expectations only partially, and the mechanism of expectation formations is described by:

pi_t^e = λ bar pi + ( 1 − λ ) pi_t−1

where the parameter λ can be thought of as meaning the extent of central bank credibility. If λ = 1, then monetary policy is entirely credible and disinflation can be pursued at zero cost. Vice versa, λ = 0 implies that monetary authorities are not credible and disinflation policy is costly.

Depression, liquidity trap, and deflation

The revised AD–AS model can be employed to describe the effect that inflation expectations may have on business cycle fluctuations. In particular, the model developed in this chapter can explain why recessions can turn into economic depressions (i.e. prolonged periods in which output is below its natural level and the unemployment rate is persistently higher than the natural rate). Panel A in Figure 4.6 illustrates the basic adjustment mechanism following an adverse demand shock which reduces output below the natural level at A 1 . In this situation the AD–AS model predicts that the economy will go through a phase of disinflation which increases real money balances. The increase in real money balances shifts the LM curve downwards until the economy converges back to the natural level of output at a lower interest rate. To understand why the recession described in panel A may turn into a depression, recall that the IS curve responds to changes in the real interest rate, whereas the LM curve responds to the nominal interest rate. In addition, the Fischer effect implies that the real interest rate is equal to the difference between the nominal interest rate and the expected inflation rate, which may also be affected by negative demand shocks. Consider the case depicted in panel B of Figure 4.6. Suppose an adverse demand shock drives output below

its natural level and the unemployment rate above the natural rate, so that the economy moves to A 1 . The Phillips curve predicts that inflation falls, so that the real money supply rises and under the basic adjustment mechanism this tends to move the economy from A 1 to A 2 . However, the fall in inflation leads also to a fall in expected inflation, which tends to increase the real interest rate for any given nominal rate. The increase in the real interest rate tends to reduce output, as it shifts the IS curve to the left and equilibrium to point B. Therefore, the net adjustment effect is, in principle, ambiguous, as it depends on whether the LM effects dominate

the IS effects. The economy could adjust along the new IS curve and return to the natural level of output at a slower pace than that predicted in panel A.

Alternatively, the economy could also continue to diverge from the natural level of output, since the increase in unemployment leads to a further fall in inflation which may reduce expected inflation even more, and in turn cause the IS curve to shift further away from equilibrium. In this scenario the effectiveness of monetary policy is limited by the fact that the nominal interest rate cannot fall below zero. In other words, monetary expansions are ineffective after the equilibrium nominal interest rate reaches zero, since the economy falls into a liquidity trap. 9 As already described in Chapter 2 of the subject guide, when the market clearing nominal interest rate is zero, the extra liquidity generated by a monetary expansion ends in a trap in the sense that people are indifferent between holding their wealth in money and bonds at the zero nominal rate. This situation implies that the segment of the LM curve corresponding to a zero nominal interest rate is flat in output-interest rate space. An increase in the nominal money supply shifts the entire LM curve to the right, so that the horizontal segment at the zero nominal interest rate gets even longer. This situation is illustrated in panel C of Figure 4.6. The short-run equilibrium is described by the intersection between the IS and the LM curves at point A 1 , so that the short run equilibrium level of output Y 1 is lower than the natural level of output. Suppose a monetary expansion shifts the LM curve to the right, so that the new equilibrium level of output Y 2 corresponds to a zero nominal interest rate. 10 Once the economy reaches the new equilibrium at A 2 any further monetary policy has no power to stimulate the economy, as an increase in the nominal money supply cannot reduce the nominal interest rate further, and output does not increase further than Y 2 .

The adjustment mechanism becomes even more complicated when people begin to expect deflation. Panel D in Figure 4.6 shows the case of an economy that is in a liquidity trap and in recession. Suppose that the economy has been in recession for some time, so that after a period of disinflation the price level begins to decrease (deflation). The deflation may lead the private sector to expect prices to further decrease in the future. As a result, the real interest rate increases, in turn reducing investment spending. The increase in the real interest rate shifts the

IS curve to the left, creating the possibility of a prolonged economic downturn. In this situation the economy gets into a vicious cycle: monetary policy is powerless and low output leads to more deflation, which in turn further reduces output via the real interest rate.

Blanchard, O., Johnson, D.R., (2013) Macroeconomics (sixth edition), Pearson

Chapter 8 The Phillips Curve, The Natural Rate of Unemployment and Inflation

In 1958, A. W. Phillips drew a diagram plotting the rate of inflation against the rate of unemployment in the United Kingdom for each year from 1861 to 1957. He found clear evidence of a negative relation between inflation and unemployment: When unemployment was low, inflation was high, and when unemployment was high, inflation was low, often even negative.

In the 1970s, however, this relation broke down. In the United States and most OECD countries, there was both high inflation and high unemployment, clearly contradicting the original Phillips curve. A relation reappeared, but it reappeared as a relation between the unemployment rate and the change in the inflation rate.

**8.1 Inflation, Expected Inflation, and Unemployment**

Our first step will be to show that the aggregate supply relation can be rewritten as a relation between inflation, expected inflation, and the unemployment rate.

P = P^e ( 1 + m) F(u,z)

Recall that the function F captures the effects on the wage of the unemployment rate, u, and of the other factors that affect wage setting represented by the catchall variable z. m is the markup of prices over wages. It will be convenient here to assume a specific form for this function:

F (u, z) = 1 - alphau + z

This captures the notion that the higher the unemployment rate, the lower the wage; and the higher z (for example, the more generous unemployment benefits are), the higher the wage. The parameter alpha captures the strength of the effect of unemployment on the wage.

Replace the function F by this specific form in the aggregate supply relation above:

P = P^e (1 + m)(1 - alphau + z) (8.1)

Finally, let p denote the inflation rate, and p^e denote the expected inflation rate.

Then equation (8.1) can be rewritten as

p = p^e + (m + z) - alphau

* An increase in expected inflation, pi^e , leads to an increase in actual inflation, pi.

* Given expected inflation, pi^e , an increase in the markup m, or an increase in the factors that affect wage determination — an increase in z—leads to an increase in inflation, pi.

* Given expected inflation, pi^e , an increase in the unemployment rate u leads to a decrease in inflation pi.

Rewriting 8.1 to account for time.

p_t = p^e_t + (m + z) - alphau_t

**8.2 The Phillips Curve**

Let’s assume that expected inflation is equal to zero—that pi^et = 0. Equation (8.3) then becomes

pi_t = (m + z) - alphau_t

This is precisely the negative relation between unemployment and inflation that Phillips found for the United Kingdom and Solow and Samuelson found for the United States.

Given the expected price level, which workers simply take to be last year’s price level, lower unemployment leads to a higher nominal wage. A higher nominal wage leads to a higher price level.... lower unemployment leads to a higher price level this year relative to last year’s price level—that is, to higher inflation. This mechanism has sometimes been called the **wage–price spiral**

* Low unemployment leads to a higher nominal wage.

* In response to the higher nominal wage, firms increase their prices. The price level increases.

* In response to the higher price level, workers ask for a higher nominal wage the next time the wage is set.

* The higher nominal wage leads firms to further increase their prices. As a result, the price level increases further.

& In response to this further increase in the price level, workers, when they set the wage again, ask for a further increase in the nominal wage.

* And so the race between prices and wages results in steady wage and price inflation.

Why did the original Phillips curve vanish? There are two main reasons:

* The United States was hit twice in the 1970s by a large increase in the price of oil. The effect of this increase in nonlabor costs was to force firms to increase their prices relative to the wages they were paying—in other words, to increase the markup m, without a change to unemployment. The main reason for the breakdown of the Phillips curve relation, however, lay elsewhere:

* Wage setters changed the way they formed their expectations. Starting in the 1960s there was a clear change in the behavior of the rate of inflation. First, rather than being sometimes positive and sometimes negative, as it had for the first part of the century, the rate of inflation became consistently positive. Second, inflation became more persistent: High inflation in one year became more likely to be followed by high inflation the next year.

* The persistence of inflation led workers and firms to revise the way they formed their expectations. When inflation is consistently positive year after year, expecting that the price level this year will be the same as the price level last year—which is the same as expecting zero inflation—becomes systematically incorrect; worse, it becomes foolish.

We can think of what happened in the 1970s as an increase in the value of theta (i.e., last year's inflation rate) over time:

pi^e_t = theta pi_t-1

When theta equals zero, we get the original Phillips curve, a relation between the inflation rate and the unemployment rate. pi_t = (m + z) - alphau_t

When theta is positive, the inflation rate depends not only on the unemployment rate but also on last year’s inflation rate. pi_t = thatpi_t-1 + (m + z) - alphau_t

When theta equals 1, the relation becomes (moving last year’s inflation rate to the left side of the equation): pi_t - pit-1 = (m + z) - alphau_t

So, when theta = 1, the unemployment rate affects not the inflation rate, but rather the change in the inflation rate: High unemployment leads to decreasing inflation; low unemployment leads to increasing inflation.

To distinguish it from the original Phillips curve (equation (8.4)), equation (8.6) or its empirical counterpart, equation (8.7) is often called the modified Phillips curve, or the expectations-augmented Phillips curve (to indicate that pi_t-1 stands for expected inflation), or the accelerationist Phillips curve (to indicate that a low unemployment rate leads to an increase in the inflation rate and thus an acceleration of the price level).

The original Phillips curve implied that there was no such thing as a natural un-employment rate: If policy makers were willing to tolerate a higher inflation rate, they could maintain a lower unemployment rate forever.

By definition, the natural rate of unemployment is the unemployment rate such that the actual price level is equal to the expected price level. Equivalently, and more conveniently here, the natural rate of unemployment is the unemployment rate such that the actual inflation rate is equal to the expected inflation

rate.

Denote the natural unemployment rate by u n (the index n stands for “natural”). Then, imposing the condition that actual inflation and expected inflation be the same

0 = ( m + z) - alphau_n, alphau_n = m

**8-3 A Summary and Many Warnings**

* The aggregate supply relation is well captured ... by a relation between the change in the inflation rate and the deviation of the unemployment rate from the natural rate of unemployment (equation (8.8))

* When the unemployment rate exceeds the natural rate of unemployment, the inflation rate typically decreases. When the unemployment rate is below the natural rate of unemployment, the inflation rate typically increases.

* In writing equation (8.6) and estimating equation (8.7), we treated m + z as a constant. But there are good reasons to believe that m and z vary over time. The degree of monopoly power of firms, the structure of wage bargaining, the system of unemployment benefits, and so on are likely to change over time, leading to changes in either m or z and, by implication, changes in the natural rate of unemployment.

What Explains European Unemployment?

What do critics have in mind when they talk about the “labor-market rigidities” afflicting Europe?

* A generous system of unemployment insurance

* A high degree of employment protection.

* Minimum wages.

* Bargaining rules.

Do these labor-market institutions really explain high unemployment in Europe? Is the case open and shut? Not quite. Fact 1: Unemployment was not always high in Europe. Until the current crisis started, a number of

European countries actually had low unemployment. Generous social protection is consistent with low unemployment. But it has to be provided efficiently.

Make sure to distinguish between deflation: a decrease in the price level (equivalently,

negative inflation), and disinflation: a decrease in the inflation rate.

Some economists argued that such a disinflation would likely be very costly. Their starting point was equation (8.10):

pi_t - pt_t-1 = - alpha(u_t - u_n)

According to this equation, the only way to bring down inflation is to accept unemployment above the natural rate for some time. We saw earlier that a is estimated to be equal to 0.55. The equation therefore implies that, to decrease inflation by one percentage point, the unemployment rate has to be higher than the natural unemployment rate by 1/0.55, or about 1.8 percentage points for a year.

Some economists argued that disinflation might in fact be much less costly. In what has become known as the Lucas critique, Lucas pointed out that when trying to predict the effects of a major policy change it could be very misleading to take as given the relations estimated from past data.

They argued that the relevant equation was not equation (8.10) but equation (8.9). And equation (8.9) implied that, if the Fed was fully credible, the decrease in inflation might not require any increase in the unemployment rate. If wage setters expected inflation to now be 4%, then actual inflation would

decrease to 4%, with unemployment remaining at the natural rate.

The essential ingredient of successful disinflation, he argued, was credibility of monetary policy—the belief by wage setters that the central bank was truly committed to reducing inflation. Only credibility would cause wage setters to change the way they formed their expectations.

Wage indexation increases the effect of unemployment on inflation. The higher the proportion of wage contracts that are indexed—the higher l—the larger the effect the unemployment rate has on the change in inflation—the higher the coefficient alpha/(1 - l). The intuition is as follows: Without wage indexation, lower unemployment increases wages, which in turn increases prices. But because wages do not respond to prices right away, there is no further increase in prices within the year. With wage indexation, however, an increase in prices leads to a further increase in wages within the year, which leads to a further increase in prices, and so on, so that the effect of unemployment on inflation within the year is higher.

If, and when, l gets close to 1—which is when most labor contracts allow for wage indexation—small changes in unemployment can lead to very large changes in inflation. Put another way, there can be large changes in inflation with nearly no change in unemployment. This is what happens in countries where inflation is very high: The relation between inflation and unemployment becomes more and more tenuous and eventually disappears altogether.

**Summary**

* The aggregate supply relation can be expressed as a relation between inflation, expected inflation, and unemployment. Given unemployment, higher expected inflation leads to higher inflation. Given expected inflation, higher unemployment leads to lower inflation.

* When inflation is not very persistent, expected inflation does not depend very much on past inflation. Thus, the aggregate supply relation becomes a relation between inflation and unemployment. This is what Phillips in the United Kingdom and Solow and Samuelson in the United States discovered when they looked, in the late 1950s, at the joint behavior of unemployment and inflation.

* As inflation became more persistent in the 1970s and 1980s, expectations of inflation became based more and more on past inflation. In the United States today, the aggregate supply relation takes the form of a relation between unemployment and the change in inflation. High unemployment leads to decreasing inflation; low unemployment leads to increasing inflation.

* The natural unemployment rate is the unemployment rate at which the inflation rate remains constant. When

the actual unemployment rate exceeds the natural rate of unemployment, the inflation rate typically decreases; when the actual unemployment rate is less than the natural unemployment rate, the inflation rate typically increases.

* The natural rate of unemployment depends on many factors that differ across countries and can change over time. This is why the natural rate of unemployment varies across countries: It is higher in Europe than in the United States. Also, the natural unemployment rate varies over time: In Europe, the natural unemployment rate has greatly increased since the 1960s. In the United States, the natural unemployment rate increased from the 1960s to the 1980s and appears to have decreased since.

* Changes in the way the inflation rate varies over time affect the way wage setters form expectations and also affects how much they use wage indexation. When wage indexation is widespread, small changes in unemployment can lead to very large changes in inflation. At high rates of inflation, the relation between inflation and unemployment disappears altogether.

* At very low or negative rates of inflation, the Phillips curve relation appears to become weaker. During the Great Depression even very high unemployment led only to limited deflation. The issue is important because many countries have both high unemployment and low inflation today.

Dornbusch, R., S. Fischer and R. Startz Macroeconomics (2011)

**Part 2: Chapter 6: Aggregate Supply: Wages, Prices, and Unemployment**

• The Phillips curve links inflation and unemployment. The aggregate supply curve links prices and output. The Phillips curve and aggregate supply curve are alternative ways of looking at the same phenomena.

• According to the modern Phillips curve, inflation depends on expectations of inflation, as well as unemployment.

The link between unemployment and inflation is called the Phillips curve. We translate between unemployment and output and also translate between inflation and price changes.

The Phillips curve is an inverse relationship between the rate of unemployment and the rate of increase in money wages. The higher the rate of unemployment, the lower the rate of wage inflation. In other words, there is a tradeoff between wage inflation and unemployment.

Something is missing from the simple Phillips curve. That something is expected, or anticipated, inflation. When workers and firms bargain over wages, they are concerned with the real value of the wage, so both sides are more or less willing to adjust the level of the nominal wage for any inflation expected over the contract period. Unemployment depends not on the level of inflation but, rather, on the excess of inflation over what was expected.

Maintaining the assumption of a constant real wage, actual inflation, pi, will equal wage inflation. Thus, the equation for the modern version of the Phillips curve, the (inflation-) expectations-augmented Phillips curve, is

pi = pi^e - epsilon (u - u^*)

Note two critical properties of the modern Phillips curve:

Expected inflation is passed one for one into actual inflation.

Unemployment is at the natural rate when actual inflation equals expected inflation.

.. the empirical relation between inflation and unemployment is a mess. We would like some evidence that adjusting for expected inflation gives us a reliable Phillips curve. Unlike inflation and unemployment, which are directly measurable and regularly reported by the official statistics agencies, expected inflation is an idea in the heads of everyone engaged in setting prices and wages... we get surprisingly good results from the naive assumption that people expect inflation this year to equal what-ever inflation was last year.

Wages are sticky, or wage adjustment is sluggish, when wages move slowly over time, rather than being fully and immediately flexible, so as to ensure full employment at every point in time.

Efficiency wage theory focuses on the wage as a means of motivating labor. The amount of effort workers make on the job is related to how well the job pays relative to alternatives. Firms may want to pay wages above the market-clearing wage to ensure that employees work hard to avoid losing their good jobs. Wages are usually set in nominal terms in economies with low rates of inflation.

The insider-outsider model predicts that wages will not respond substantially to unemployment and thus offers another reason why we do not quickly return to full employment once the economy experiences recession.

Work back from the Phillips curve to the aggregate supply curve. The derivation will take four steps. First, we translate output to employment. Second, we link the prices firms charge to their costs. Third, we use the Phillips curve relationship between wages and employment. Fourth, we put the three components together to derive an upward-sloping aggregate supply curve.

Summary

* The labor market does not adjust quickly to disturbances. Rather, the adjustment process takes time. The Phillips curve shows that nominal wages change slowly in accordance with the level of employment. Wages tend to rise when employment is high and fall when employment is low.

* Expectations of inflation are built into the Phillips curve. When actual inflation and expected inflation are equal, the economy is at the natural rate of unemployment.

* Expectations of inflation adjust over time to reflect the recent levels of inflation.

* Stagflation occurs when there is a recession plus a high inflation rate. That is, stagflation occurs when the economy moves to the right along a Phillips curve that includes a substantial component of expected inflation.

* The short-run Phillips curve is quite flat. Within a year, one point of extra unemployment reduces inflation by only about one-half of a point of inflation.

* Rational expectations theory argues that the aggregate supply curve should shift very quickly in response to anticipated changes in aggregate demand, so output should change relatively little.

* The frictions that exist as workers enter the labor market and look for jobs or shift between jobs mean that there is always some frictional unemployment. The amount of frictional unemployment that exists at the full-employment level of unemployment is the natural rate of unemployment.

* The theory of aggregate supply is not yet settled. Several explanations have been offered for the basic fact that the labor market does not adjust quickly to shifts in aggregate demand: the imperfect-information–market-clearing approach; coordi-nation problems; efficiency wages and costs of price changes; and contracts and long-term relationships between firms and workers.

* In deriving the supply curve in this chapter, we emphasize the long-run relationships between firms and workers and the fact that wages are generally held fixed for some period, such as a year. We also take into account the fact that wage changes are not coordinated among firms.

* The short-run aggregate supply curve is derived from the Phillips curve in four steps: Output is assumed proportional to employment; prices are set as a markup over costs; the wage is the main element of cost and adjusts according to the Phillips curve; and the Phillips curve relationship between the wage and unemployment is therefore transformed into a relationship between the price level and output.

* The short-run aggregate supply curve shifts over time. If output is above (below) the full-employment level this period, the aggregate supply curve shifts up (down) next period.

* A shift in the aggregate demand curve increases the price level and output. The increase in output and employment increases wages somewhat in the current period. The full impact of changes in aggregate demand on prices occurs only over the course of time. High levels of employment generate increases in wages that feed into higher prices. As wages adjust, the aggregate supply curve shifts until the economy returns to equilibrium

* The aggregate supply curve is derived from the underlying assumptions that wages (and prices) are not adjusted continuously and that they are not all adjusted together. The positive slope of the aggregate supply curve is a result of some wages being adjusted in response to market conditions and of previously agreed-on overtime rates coming into effect as employment changes. The slow movement of the supply curve over time is a result of the slow and uncoordinated process by which wages and prices are adjusted.

* Materials prices (oil price, for example), along with wages, are determinants of costs and prices. Changes in materials prices are passed on as changes in prices and, therefore, as changes in real wages. Materials price changes have been an important source of aggregate supply shocks.

* Supply shocks pose a difficult problem for macroeconomic policy. They can be accommodated through an expansionary aggregate demand policy, with increased prices but stable output. Alternatively, they can be offset, through a deflationary aggregate demand policy, with prices remaining stable but with lower output.

* Favorable supply shocks appear to explain rapid growth at the end of the 20th century. Wise aggregate demand policy in the presence of favorable supply shocks can provide rapid growth with low inflation.

Part 2: Chapter 7

• The costs of unemployment, mainly forgone output, are very large.

• The cost of anticipated inflation is very small, at least at the moderate levels experienced in industrial countries.

• The cost of unanticipated inflation, which can be quite large, is mainly distributional. There are big winners and big losers.

• Unemployment rates, both the natural rate and the rate of cyclical unemployment, vary widely among different groups and countries.

In the short run, governments can reduce inflation only at the cost of increased unemployment and reduced output. The sacrifice ratio is the percentage of output lost for each 1 point reduction in the inflation rate. The sacrifice ratio varies depending on the time, place, and methods used to reduce inflation.

The largest single cost of unemployment is lost production. The cost of lost output is very high: A recession can easily cost 3 to 5 percent of GDP.. Okun’s law states that 1 extra point of unemployment costs 2 percent of GDP. The costs of unemployment are borne very unevenly. There are large distributional consequences. In other words, the costs of a recession are borne disproportionately by those individuals who lose their jobs.

The costs of extremely high inflation are easy to see. Unexpected inflation has an easily seen distributional cost: Debtors benefit by repaying in cheaper dollars, and creditors suffer by being repaid in cheaper dollars.

CYCLICAL AND FRICTIONAL UNEMPLOYMENT

There is an important distinction between cyclical and frictional unemployment. Frictional unemployment is the unemployment that exists when the economy is at full employment. Frictional unemployment results from the structure of the labor market—from the nature of jobs in the economy and from the social habits and labor market institutions (e.g., unemployment benefits) that affect the behavior of workers and firms. The frictional unemployment rate is the same as the natural unemployment rate, which we discuss in more detail below. Cyclical unemployment is unemployment in excess of frictional unemployment: It occurs when output is below its full-employment level.

The notion of full employment—or the natural, or frictional, rate of unemployment—plays a central role in macroeconomics and also in macroeconomic policy.

Suppose that an economy has been experiencing a given rate of inflation, say, 5 percent, for a long time and that everyone correctly anticipates that the rate of inflation will continue to be 5 percent. In such an economy, all contracts would build in the expected 5 percent inflation. n such an economy, inflation has no real costs—except for two qualifications. The first qualification arises because no interest is paid on currency—notes and coins—not least because it is very difficult to do so. This means that the costs of holding currency rise along with the inflation rate. Plus... The costs of these trips to the bank are often described as the “shoe-leather” costs of inflation. Plus ... the menu costs of inflation.

The public dislikes both unemployment and inflation. One attempt to measure the political effect of unemployment and inflation is called the misery index, which is simply the sum of unemployment and inflation... a weak negative relation between the change in the misery index and the fortunes of the incumbent’s party. But as you can gather from the figure, the evidence for the relation is hardly overwhelming. In part, this is because so many other factors also drive voters’ decisions. In addition, voters probably do not weigh unemployment and inflation equally—as the misery index does implicitly.

Misery index = u + pi

p178

SUMMARY

* The anatomy of unemployment in the United States reveals frequent short spells of unemployment. Nonetheless, a substantial fraction of U.S. unemployment is accounted for by those who are unemployed for a large portion of time.

* There are significant differences in unemployment rates across age groups and race. Unemployment among black teenagers is highest, and that among white adults is lowest. The young and minorities have significantly higher unemployment rates than middle-aged whites.

* The concept of the natural, or frictional, rate of unemployment singles out the part of unemployment that would exist even at full employment. This unemployment arises from the natural frictions of the labor market, as people move between jobs. The natural rate is hard to measure, but the consensus is to estimate it at about 5.5 percent, up from the 4 percent of the mid-1950s. The official (CBO) estimate is 4.8 percent.

* Policies to reduce the natural rate of unemployment involve structural labor market policies. Disincentives to employment and training, such as minimum wages, and incentives to extended job search, such as high unemployment benefits, tend to raise the natural rate. It is also possible that unemployment dis plays hysteresis, with extended periods of high unemployment raising the natural rate.

* The costs of unemployment are the psychological and financial distress of the unemployed, as well as the loss of output. In addition, higher unemployment tends to hit the poorer members of society disproportionately.

* The economy can adjust to perfectly anticipated inflation by moving to a system of indexed taxes and to nominal interest rates that reflect the expected rate of inflation. If inflation were perfectly anticipated and adjusted to, the only costs of inflation would be shoe-leather and menu costs.

* Imperfectly anticipated inflation has important redistributive effects among sectors. Unanticipated inflation benefits monetary debtors and hurts monetary creditors. The government gains real tax revenue, and the real value of government debt declines.

* In the U.S. housing market, unanticipated increases in inflation, combined with the tax deductibility of interest, made housing a particularly good investment during the 1960–1980 period.

* In the U.S. economy, indexation is neither very widespread nor complete. The absence of strong indexation probably eased the adjustment to supply shocks.

* While very high inflation rates are bad, there is some evidence that a small positive inflation rate lubricates the economy by reducing real wage rigidity.

* The political business cycle hypothesis emphasizes the economy’s direction of change. For incumbents to win an election, the unemployment rate should be falling and the inflation rate not worsening.

Mankiw, N. G. Macroeconomics. (Worth, 2009)

Chapter 6

Any policy aimed at lowering the natural rate of unemployment must either reduce the rate of job separation or increase the rate of job finding. Similarly, any policy that affects the rate of job separation or job finding also changes the natural rate of unemployment.

The unemployment caused by the time it takes workers to search for a job is called frictional unemployment.

A second reason for unemployment is wage rigidity—the failure of wages to adjust to a level at which labor supply equals labor demand. In the equilibrium model of the labor market, the real wage adjusts to

equilibrate labor supply and labor demand. Sometimes the real wage is stuck above the market-clearing level. The unemployment resulting from wage rigidity and job rationing is sometimes called structural unemployment.

The government causes wage rigidity when it prevents wages from falling to equilibrium levels. Minimum-wage laws set a legal minimum on the wages that firms pay their employees. Economists believe that the minimum wage has its greatest impact on teenage unemployment.

Efficiency-wage theories propose a third cause of wage rigidity in addition to minimum-wage laws and unionization. These theories hold that high wages make workers more productive. The influence of wages on worker efficiency may explain the failure of firms to cut wages despite an excess supply of labor. Even though a wage reduction would lower a firm’s wage bill, it would also—if these theories are correct—lower worker productivity and the firm’s profits.

One efficiency-wage theory, which is applied mostly to poorer countries, holds that wages influence nutrition. Better-paid workers can afford a more nutritious diet, and healthier workers are more productive.

A second efficiency-wage theory, which is more relevant for developed countries, holds that high wages reduce labor turnover.

A third efficiency-wage theory holds that the average quality of a firm’s work force depends on the wage it pays its employees.

A fourth efficiency-wage theory holds that a high wage improves worker effort.

Summary

1. The natural rate of unemployment is the steady-state rate of unemployment. It depends on the rate of job separation and the rate of job finding.

2. Because it takes time for workers to search for the job that best suits their individual skills and tastes, some frictional unemployment is inevitable. Various government policies, such as unemployment insurance, alter the amount of frictional unemployment.

3. Structural unemployment results when the real wage remains above the level that equilibrates labor supply and labor demand. Minimum-wage legislation is one cause of wage rigidity. Unions and the threat of unionization are another. Finally, efficiency-wage theories suggest that, for various reasons, firms may find it profitable to keep wages high despite an excess supply of labor.

4. Whether we conclude that most unemployment is short-term or long-term depends on how we look at the data. Most spells of unemployment are short. Yet most weeks of unemployment are attributable to the small number of long-term unemployed.

5. The unemployment rates among demographic groups differ substantially. In particular, the unemployment rates for younger workers are much higher than for older workers. This results from a difference in the rate of job separation rather than from a difference in the rate of job finding.

6. The natural rate of unemployment in the United States has exhibited long-term trends. In particular, it rose from the 1950s to the 1970s and then started drifting downward again in the 1990s and early 2000s. Various explanations of the trends have been proposed, including the changing demographic composition of the labor force, changes in the prevalence of sectoral shifts, and changes in the rate of productivity growth.

7. Individuals who have recently entered the labor force, including both new entrants and reentrants, make up about one-third of the unemployed. Transitions into and out of the labor force make unemployment statistics more difficult to interpret.

8. American and European labor markets exhibit some significant differences. In recent years, Europe has experienced significantly more unemployment than the United States. In addition, because of higher unemployment, shorter workweeks, more holidays, and earlier retirement, Europeans work fewer hours than Americans.

Chaper 13: Aggregate Supply and the Short-Run Tradeoff Between Inflation and Unemployment

Examining two prominent models of aggregate supply. In both models, some market imperfection (that is, some type of friction) causes the output of the economy to deviate from its natural level. As a result, the short-run aggregate supply curve is upward sloping rather than vertical, and shifts in the aggregate demand curve cause output to fluctuate. These temporary deviations of output from its natural level represent the booms and busts of the business cycle.

Each of the two models takes us down a different theoretical route, but each route ends up in the same place. That final destination is a short-run aggregate supply equation of the form

Y = barY + alpha(P − EP), alpha> 0,

where Y is output, barY is the natural level of output, P is the price level, and EP is the expected price level. This equation states that output deviates from its nat ural level when the price level deviates from the expected price level. The parameter a indicates how much output responds to unexpected changes in the

price level; 1/alpha is the slope of the aggregate supply curve.

The most widely accepted explanation for the upward-sloping short-run aggregate supply curve is called the sticky-price model. This model emphasizes that firms do not instantly adjust the prices they charge in response to changes in demand.

Another explanation for the upward slope of the short-run aggregate supply curve is called the imperfect-information model. Unlike the previous model, this one assumes that markets clear—that is, all prices are free to adjust to balance supply and demand. In this model, the short-run and long-run aggregate supply curves differ because of temporary misperceptions about prices.

When Robert Lucas proposed the imperfect-information model, he derived a surprising interaction between aggregate demand and aggregate supply: according to his model, the slope of the aggregate supply curve should depend on the volatility of aggregate demand. In countries where aggregate demand fluctuates widely, the aggregate price level fluctuates widely as well. Lucas tested this prediction by examining international data on output and prices. He found that changes in aggregate demand have the biggest effect on output in those countries where aggregate demand and prices are most stable. Lucas concluded that the evidence supports the imperfect-information model.

The Short-Run Aggregate Supply Curve Output deviates from its natural − level Y if the price level P

deviates from the expected price level EP.

The Phillips curve in its modern form states that the inflation rate depends on

three forces:

* Expected inflation

* The deviation of unemployment from the natural rate, called cyclical unemployment

* Supply shocks.

These three forces are expressed in the following equation:

pi - Epi - beta(u - u^n) + v

The second and third terms in the Phillips curve equation show the two forces that can change the rate of inflation. Low unemployment pulls the inflation rate up. This is called demand-pull inflation because high aggregate demand is responsible for this type of inflation. High unemployment pulls the inflation rate down.

An adverse supply shock, such as the rise in world oil prices in the 1970s, implies a positive value of and causes inflation to rise. This is called cost-push inflation because adverse supply shocks are typically events that push up the costs of production. A beneficial supply shock, such as the oil glut that led to a

fall in oil prices in the 1980s, makes negative and causes inflation to fall.

Summary

1. The two theories of aggregate supply—the sticky-price and imperfect-information models—attribute deviations of output and employment from their natural levels to various market imperfections. According to both theories, output rises above its natural level when the price level exceeds the expected price level, and output falls below its natural level when the price level is less than the expected price level.

2. Economists often express aggregate supply in a relationship called the Phillips curve. The Phillips curve says that inflation depends on expected inflation, the deviation of unemployment from its natural rate, and supply shocks. According to the Phillips curve, policymakers who control aggregate demand face a short-run tradeoff between inflation and unemployment.

3. If expected inflation depends on recently observed inflation, then inflation has inertia, which means that reducing inflation requires either a beneficial supply shock or a period of high unemployment and reduced output. If people have rational expectations, however, then a credible announcement of a change in policy might be able to influence expectations directly and, therefore, reduce inflation without causing a recession.

4. Most economists accept the natural-rate hypothesis, according to which fluctuations in aggregate demand have only short-run effects on output and unemployment. Yet some economists have suggested ways in which recessions can leave permanent scars on the economy by raising the natural rate of unemployment.